On 1 March 2014, SIX Exchange Regulation’s revised Directive on Delisting came into force. The introduction of a shareholders’ right to challenge the period set between the delisting announcement and the last day of trading is probably the most significant change. Such period may be set by the SIX Exchange Regulation between 3 and 12 months with a view to providing shareholders the possibility to sell their stock on-exchange prior to delisting. The issuer is no longer obliged to provide for off-exchange trading after the delisting. A few months after entering into force, the revised Directive on Delisting has been tested in three instances which provide insight into how SIX Exchange Regulation intends to apply the rules.

By Mariel Hoch/Thomas Reutter (Reference: CapLaw-2014-22)

1) Introduction

The revised Directive on Delisting of Equity Securities, Derivatives and Exchange Traded Products (Delisting Directive) governing the delisting of equity securities (as well as derivatives and exchange traded products) from the principal Swiss stock exchange, the SIX Swiss Exchange, became effective on 1 March 2014. The Delisting Directive sets out the procedure and requirements an issuer must fulfi ll in order to delist its equity securities.

Delistings initiated by the issuer (i.e. all cases other than delistings under SIX Exchange Regulation’s sanctions regime) can be divided into two main categories: (i) delistings where an issuer decides to forego the benefits of an arguably easier access to capital markets provided by a listing and to save the cost of being listed (Ordinary Delistings) and (ii) delistings which occur once an issuer has no or very few shareholders left, which is usually the case following a public tender offer, a merger or liquidation (Qualified Delistings). Ordinary Delistings have a greater impact on a shareholder’s position than Qualified Delistings given that the actions preceding Qualified Delistings typically provide for special protections of shareholders’ financial position and/or exit rights (e.g. the right to tender the shares into a public tender offer and/or the right to a fair price and/or the requirement of shareholder consent). In Ordinary Delisting situations shareholders of Swiss issuers do not benefit from specific protection, but the board of directors of an issuer who delists must observe certain principles of corporate law (i.e. act in the best interest of the company).

2) The delisting decision under increased scrutiny

The Delisting Directive stipulates and has always stipulated that, except for cases where SIX Exchange Regulation may delist an issuer by way of a sanction for noncompliance with the Listing Rules, the decision to delist rests with the issuer (article 3 para 1 Delisting Directive). The question which body corporate is competent to decide on an issuer’s delisting is, however, not governed by the Delisting Directive. Swiss corporate law (the Swiss Code of Obligations) applies if the issuer has its registered seat in Switzerland. Swiss corporate law provides for the competence of the board of directors on delisting matters. Corporate law would, however, allow Swiss issuers to shift such competence to the shareholders’ meeting by introducing a respective provision in the articles of association or by seeking shareholders’ approval to the board of directors’ plans to delist. Regarding foreign issuers with a SIX listing, the applicable law to define the competent corporate body must be determined according to international private law.

In the recent past, minority shareholders have become more vocal in their objections to delisting decisions. For example, certain shareholders of Edisun Power Europe AG have expressed their discontent with the board’s decision to delist at the shareholders’ meeting of 11 May 2014. In certain instances, shareholders have tried to challenge decisions to delist before SIX Exchange Regulation’s Appeals Board and Arbitral Tribunal as well as before ordinary courts. For example, a shareholder of Petroplus Holdings AG tried to appeal the SIX Exchange Regulation’s delisting decision in 2012 and in 2010 the Swiss Federal Court had to decide on a question of jurisdiction raised by a shareholder of delisted Lenzerheide Bergbahnen AG.

3) Key changes in the revised Delisting Directive

Against the background of this increasingly contentious environment for delistings the SIX Exchange Regulation has enacted the following principal changes to the Delisting Directive:

a) Content of delisting request

The revised Delisting Directive requires the issuer to motivate its request in particular with respect to the requested period between announcement and last trading day (see below section 3)c)). A declaration of the issuer that the competent body corporate (board of directors or shareholders’ meeting respectively) has approved the delisting must be included in the exhibits to the request.

b) Publication of delisting decision

Under the previous rules, SIX Exchange Regulation did not publish its delisting decisions and provided a motivation to the issuer only upon the issuer’s express request against a fee.

Under the revised Delisting Directive, SIX Exchange Regulation publishes its decisions on delistings, including its motivation, on its website and in a media release (article 4 para 2 Delisting Directive). Such publication is necessary to allow shareholders to make use of their new appeal right (see below section 3)d)). Since the revised regime came into force on 1 March 2014, SIX Exchange Regulation has approved the delistings of the equity securities of Weatherford International Ltd (decision of 2 May 2014), PG&E Corporation (decision of 19 May 2014) and Absolute Invest AG (decisions of 15 and 19 May 2014). The motivations of the decisions so far issued are rather short. The issuer must publish relevant information on the delisting in an official notice (article 4 para 2 Delisting Directive) and, if applicable, an ad hoc statement (article 53 et seq Listing Rules). A delisting advertisement is no longer required.

c) Period between announcement and last trading day

Under the revised rules, the period between the delisting announcement and the last trading day may be no less than three and no more than 12 months for Ordinary Delistings. When determining the exact length of the period, SIX Exchange Regulation will take into account various aspects such as timing, free float, liquidity, trading volume or shareholders’ approval, if applicable.

In situations of Qualifi ed Delistings, SIX Exchange Regulation may shorten such period to as little as five trading days (i.e. following mergers, public tender offers, statutory squeeze outs, etc). This possibility has remained unchanged compared to the previous rules.

Given the possibility of SIX Exchange Regulation to extend the period between the delisting announcement and the last trading day to up to 12 months, the obligation of the issuer to provide for off-exchange trading of up to six months following delisting has been abolished. The key difference between the previous obligation to provide for off-exchange trading and the newly introduced longer period between announcement of the delisting and the last trading day is that under the new rules the issuer will continue to be bound by the Listing Rules (such as regular reporting obligations, ad hoc publicity rules, reporting of management transactions etc.) and other statutory provisions applicable only to listed companies (such as say on pay rules) until the period ends.

Should SIX Exchange Regulation start to routinely set the period at the longer end of the three-to-twelve-months range, this would mean a significant prolongation of the delisting process (even if one includes the six months period of off-exchange trading under the previous rules).

d) Shareholders’ right to appeal

Shareholders have the right to challenge the delisting decision of SIX Exchange Regulation regarding the duration between the delisting announcement and the last day of trading. Such appeal must be brought before the Appeal Board (article 62 para 3 Listing Rules). Shareholders need to demonstrate that they have an interest worthy of protection in having the decision amended. Shareholders have no right to challenge other aspects of SIX Exchange Regulation’s delisting decision such as the fundamental question whether or not a delisting is in the interest of the company or its shareholders. Depending on the circumstances of the case, such discontent can potentially be the subject matter of a liability claim against members of the board of directors.

The appeal period ends 20 trading days following the publication of SIX Exchange Regulation’s delisting decision. The appeal decision of the Appeal Board may not be challenged before the Board of Arbitration.

In situations of Qualifi ed Delistings, i.e. where the period between the announcement and the last trading day may be reduced to as little as five trading days, a shareholder must immediately request that his appeal be granted suspensive effect in order not to frustrate the requested outcome of his appeal, i.e. a longer trading period before delisting takes effect. If the Appeal Board grants such suspensive effect, the timing of such Qualified Delistings will be significantly extended as appeals procedures may take several months. Issuers may request a conditional delisting decision early on to have the appeals procedure start as soon as the transaction (i.e. a public tender offer or a merger) is announced.

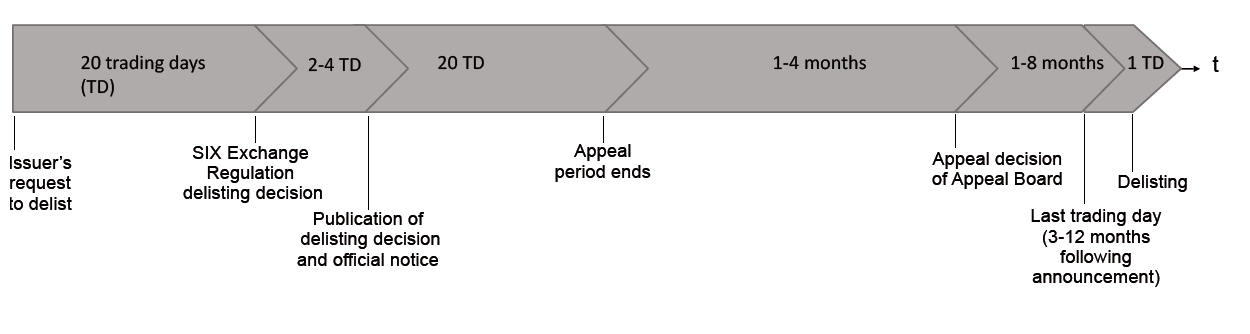

4) Summary of timeline

The provisions of the revised Delisting Directive lead to the following summary timeline if an appeal is lodged:

5) Outlook

With the exemption of the abolishment of the requirement to warrant off-exchange trading following delisting, the revised rules are more restrictive on the issuer and significantly reduce predictability of the delisting process since shareholders are granted the right to appeal the delisting decision and to so potentially stretch the delisting date by several months.

For issuers and bidders for SIX Swiss Exchange listed targets, the new appeal right of shareholders leads to increased uncertainty regarding the issuer’s ability to effectively plan and implement the delisting process because it allows shareholders to derail such process, which under the previous regime enjoyed a high level of predictability.

Mariel Hoch (mariel.hoch@baerkarrer.ch)

Thomas Reutter (thomas.reutter@baerkarrer.ch)