Under current Swiss law, portfolio managers, unless they are acting as asset managers for collective investment schemes, and trustees are not subject to a comprehensive prudential supervision, a situation that will change under the proposed new Financial Institutions Act (“FinIA”). On 14 December 2016, this proposed new act took the first parliamentary hurdle when the Swiss Council of States deliberated and passed the new act. Compared to the draft bill published by the Swiss government in November 2015 (see CapLaw 2016-8), the draft FinIA now passed by the Swiss Council of States includes a number of significant changes to the new supervisory framework applicable to portfolio managers and trustees. Most notably, portfolio managers and trustees will have to apply for a license with the Swiss Financial Market Supervisory Authority (FINMA), while the ongoing (day-to-day) prudential supervision of these financial institutions will fall within the responsibility of new private supervisory organizations.

By Patrick Schleiffer / Patrick Schärli (Reference: CapLaw-2017-07)

1) Portfolio Managers and Trustees will be FINMA-licensed Entities

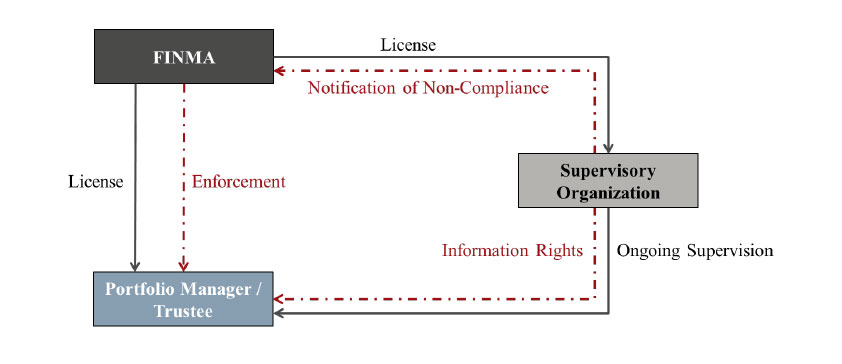

Unlike as originally suggested by the Swiss Federal Council in its draft bill of November 2015 (see CapLaw 2016-8), the Swiss Council of States now proposes in its draft of the FinIA that portfolio managers and trustees will be required to obtain their license from FINMA and not from the relevant supervisory organizations. The supervisory organizations will, however, be responsible for the ongoing (day-to-day) prudential supervision of portfolio managers and trustees.

Overview of the new supervisory regime as proposed by the Swiss Council of States:

a) Scope of the New Rules

The FinIA will, for the first time, subject portfolio managers and trustees to license requirements and an ongoing prudential supervision. Under current law, these types of financial intermediaries were only required to register themselves with a self-regulatory organization (“SRO”) for purposes of compliance with the Swiss anti-money laundering laws and, if acting as portfolio manager in relation to funds, also with an industry organization for independent portfolio managers recognized by FINMA. The draft FinIA defines portfolio managers as someone that, based on a mandate agreement, can dispose of a client’s asset by way of the following activities: (i) purchase or sale of financial instruments, (ii) acceptance and transmission of client orders relating to financial instruments, (iii) management of financial instruments, or (iv) advice relating to financial instruments. A trustee is defined as someone that based on a trust deed can dispose of the assets of a trust within the meaning of the Hague Trust Convention.

b) License Requirements

The draft FinIA (as passed by the Swiss Council of States) also provides for detailed list of prerequisites that need to be met by applicants for a trustee or portfolio manager license. In particular, the Swiss Council of State added the following additional licensing prerequisites to the draft FinIA:

- The management of a portfolio manager or a trustee must be composed of at least two qualified individuals. An individual is qualified within the meaning of the draft FinIA if such individual has an adequate education and sufficient professional experience when taking over the management of a portfolio manager or a trustee. The details will be set out in the Federal Council’s ordinance to the FinIA.

- A portfolio manager or a trustee will have to implement an adequate risk management and effective internal controls, including a compliance function. Risk management and compliance functions have to be independent from the business side. These functions may, however, be delegated to qualified third parties.

- Portfolio managers and trustees will be required to have a minimum capital of CHF 100,000. In addition, they need to maintain additional equity in an amount equal to one quarter of their fixed costs, but no more than CHF 10,000,000.

c) Ongoing Supervision and Audit of Portfolio Managers and Trustees

As mentioned above, the ongoing prudential supervision of portfolio managers and trustees will be the responsibility of the new privately organized supervisory organizations. These supervisory organizations may conduct audits of portfolio managers and trustees themselves or they can require the portfolio managers and trustees to appoint an external auditor for purposes of the regulatory audit. This rule will allow the existing industry organizations and/or SROs with their own audit organization to continue to conduct their own audits (should such organization decide to apply for a license as supervisory organization).

The supervisory organization will have the possibility to reduce the audit frequency of the portfolio managers and trustees supervised by them. This risk-based approach allows smaller entities to benefit from a reduced supervisory burden. In years where there is no audit, the supervised entities will have to prepare and file a (standardized) report on their compliance with the relevant laws and regulations.

2) Supervisory Organizations

Under the FinIA, the privately organized supervisory organizations which must have their registered seat in Switzerland will be responsible for the ongoing (day-to-day) supervision of portfolio managers and trustees. The draft FinIA which will amend the existing Financial Markets Supervisory Act (FINMASA) explicitly provides that there may be more than one supervisory organization.

The already existing industry organizations for independent portfolio managers are the most likely candidates for becoming a supervisory organization of portfolio managers. Already today, these industry organizations implement rules and procedures for the supervision of their members (e.g. through their FINMA-recognized minimum standards for portfolio management services). It is to be expected that a number of these industry organizations and/or the existing SROs will try to obtain an authorization as a supervisory organization.

In addition to the supervision of portfolio managers and trustees, a supervisory organization may also act (or continue to act) as a SRO for the purpose of anti-money laundering supervision of financial intermediaries that themselves are not required to obtain a license under the FinIA.

a) FINMA Authorization

Acting as a supervisory organization requires authorization from FINMA. FINMA will have to decide on an authorization application within one year of the entry into force of the FinIA, provided, however, the application was submitted to FINMA within six months of the entry into force of the amended FINMASA.

b) Powers

As mentioned above, the supervisory organizations will be responsible for the ongoing (day-to-day) prudential supervision of portfolio managers and trustee. Should a supervisory organization learn that a portfolio manager or a trustee does not comply with its obligations, it can set a deadline within which the respective portfolio manager or trustee has to remedy the situation. Other than that and a general right to obtain information from the supervised entities, the supervisory organizations do not have any other supervisory or enforcement tools at their disposal. In particular, the supervisory organizations will not be able to open their own enforcement action. Accordingly, if a supervised entity does not comply with its duties, the supervisory organizations will have to notify FINMA who will then take up appropriate enforcement actions.

3) Transitional periods

In addition to significantly changing the future regulatory framework applicable to portfolio managers and trustees, the Swiss Council of States also extended the transitional periods with respect to financial institutions that will be newly subject to licensing and prudential supervision under the FinIA. While these financial institutions still have to notify FINMA within six months of the entry into force, they now have up to three years to reorganize and meet the new requirements of the FinIA; provided, however, they already are and remain a member of a SRO.

The draft FinIA now also provides for transitional periods with respect to portfolio managers and trustees that will start their business after the entry into force of the FinIA, but before a supervisory organization has been authorized by FINMA. While these new portfolio managers and trustees will have to notify FINMA and meet the licensing requirements (with the exception of the membership in a supervisory organization) right away, they will only have to file a licensing application once a supervisory organization has been authorized. Until then, they may be acting as a portfolio manager or trustee, provided they are a member of a SRO.

4) Conclusion

The draft FinIA as passed by the Swiss Council of States provides for a number of significant changes to the regulatory regime that will be applicable to portfolio managers and trustees in the future. By amending the draft and transferring powers from the supervisory organizations to FINMA, the Swiss Council of States has created a coherent licensing and enforcement regime applicable to all types of financial intermediaries. Further, the regulatory regime as passed by the Swiss Council of States allows the currently existing industry organizations for independent portfolio managers and/or SROs to more easily transform into supervisory organizations and it provides for significantly more flexibility in terms of how audits of portfolio managers and trustees will be carried out.

Patrick Schleiffer (patrick.schleiffer@lenzstaehelin.com)

Patrick Schärli (patrick.schaerli@lenzstaehelin.com)