A bond issued by a foreign resident issuer but guaranteed by its Swiss resident parent company is reclassified as a domestic issuance and subject to 35 percent withholding tax if the proceeds raised under such bond are used in Switzerland. According to new rules which entered into force on 1 April 2017, it is possible to use the proceeds in Switzerland up to an amount equal to the equity of the foreign issuer and to still avoid a reclassification.

By Stefan Oesterhelt (Reference: CapLaw-2018-01)

1) Introduction

Switzerland levies a 35 percent withholding tax (Verrechnungssteuer) on interest payments with respect to bonds. International capital markets generally do not accept bond issuances subject to such deduction of Swiss withholding tax. As a consequence, it is common for Swiss multinational groups to issue bonds through a foreign subsidiary. This is accepted by the Swiss federal tax administration as long as the proceeds raised under such foreign issuance are used outside of Switzerland at all times while the bonds are outstanding. New rules which entered into force on 1 April 2017 added additional flexibility in this respect.

2) General Principles

A bond issued by an entity resident outside of Switzerland will be (re-)characterized as domestic issuance if such bond is guaranteed by the Swiss parent company and the proceeds from the issuance are used in Switzerland. In such a case, the Swiss guarantor will have to pay 35 percent Swiss withholding tax on any interest payments (53.8 percent in case of a gross-up) to the Swiss federal tax administration.

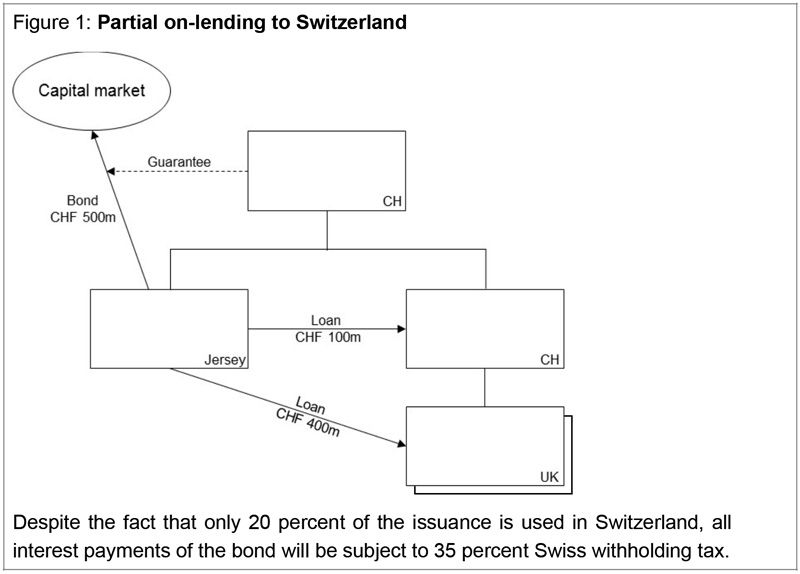

Any direct or indirect on-lending to a Swiss group company is considered as a potentially harmful “use of proceeds in Switzerland” for these purposes. In the case of such an “use of proceeds” in Switzerland, the bond will be reclassified in its entirety as a domestic issuance (see Figure 1).

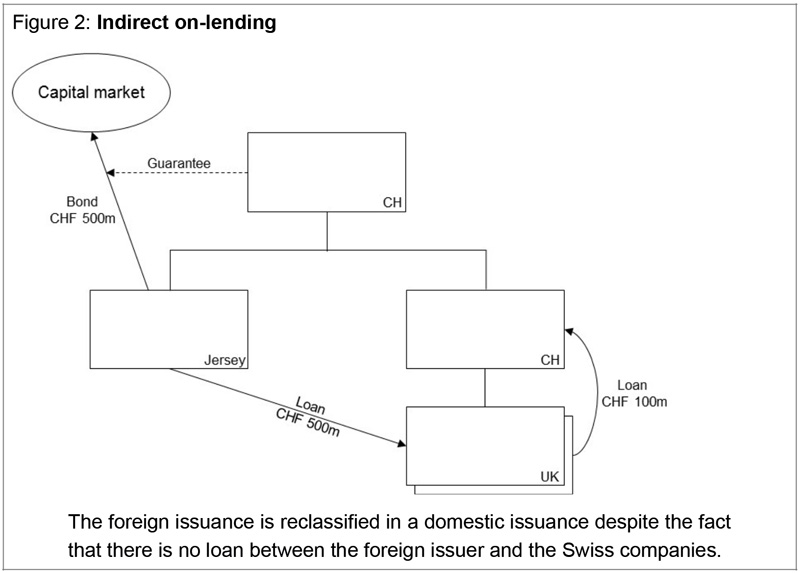

A foreign bond is reclassified in a domestic issuance subject to withholding tax even if there is no direct on-lending to Switzerland but an indirect on-lending to Switzerland (see Figure 2).

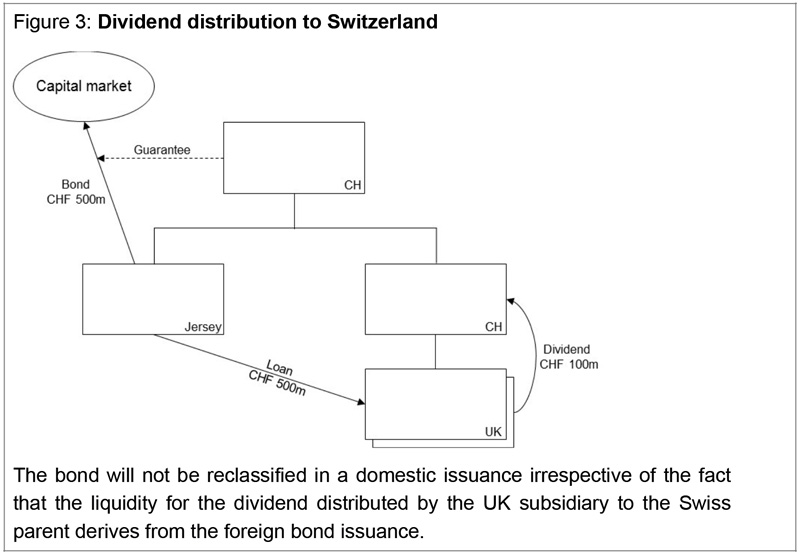

A use of proceeds in Switzerland is only potentially harmful if there is a (direct or indirect) on-lending to Switzerland. Equity contributions or dividend distributions are not harmful (see Figure 3).

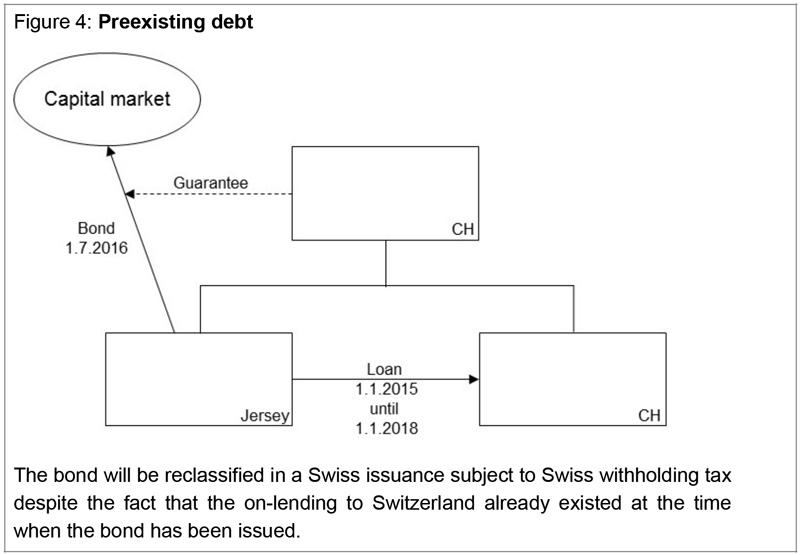

A connection between the foreign bond issuance and the on-lending to Switzerland is not necessary for such a reclassification of the bond. Even pre-existing on-lending to Switzerland is potentially harmful (see Figure 4).

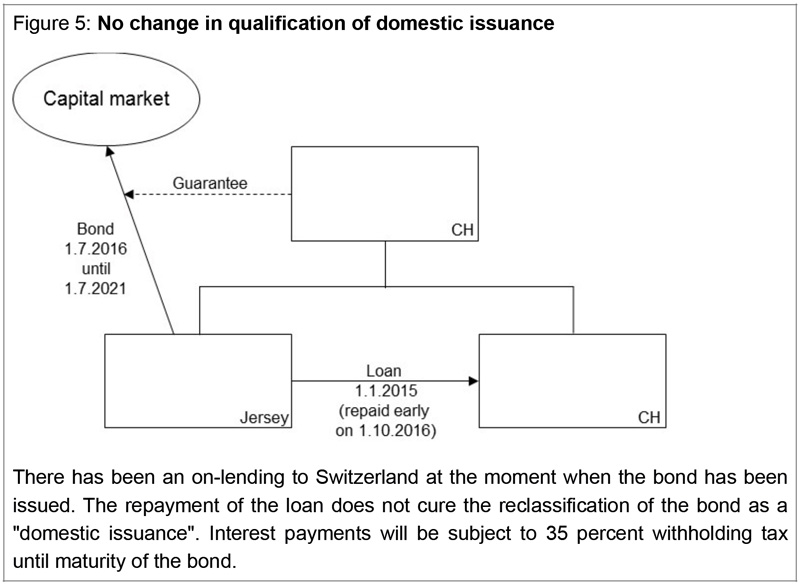

Once there has been a harmful “use of proceeds in Switzerland” and consequently a bond has to be reclassified as a domestic issuance, the bond will keep this classification until maturity (see Figure 5). A repayment of the on-lending to Switzerland does not cure the reclassification.

3) New Rules

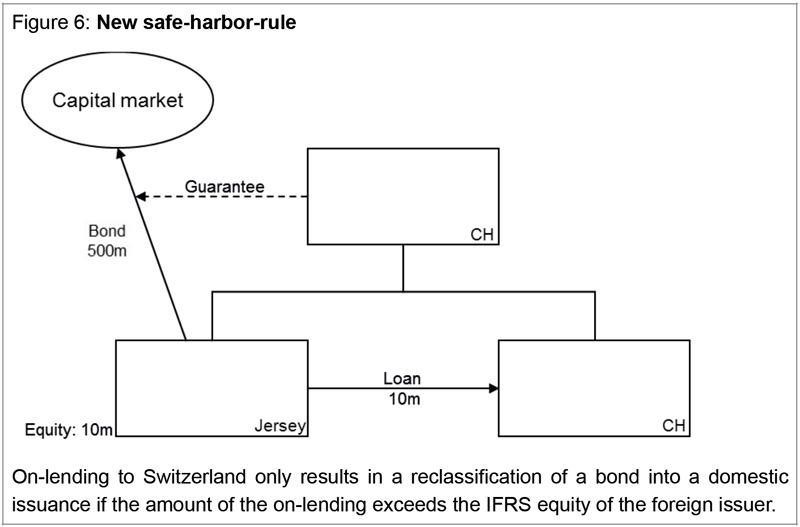

The rules which entered into force on 1 April 2017 introduce a new safe harbor rule for on-lending into Switzerland. Under this rule, it is permissible to on-lend to Switzerland up to an amount equal to the amount of the equity of the foreign issuer (see Figure 6).

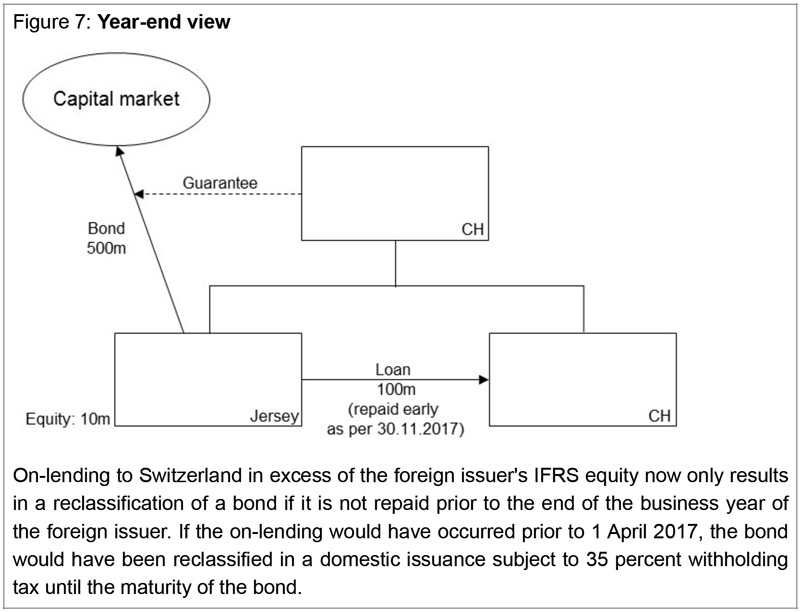

Under the new rules, the equity of the foreign issuer at the end of the business year of the foreign issuer is decisive. Consequently, any on-lending to Switzerland which is repaid before year-end is not harmful (see Figure 7).

The new rule is subject to the abuse of law principle, however. The Swiss Federal Tax Administration would still reclassify a bond into a domestic issuance if the proceeds of the bond are used in Switzerland most of the time (but never over year-end date).

4) Appraisal

The general rule that on-lending to Switzerland is not permissible if a foreign issued bond is guaranteed by a Swiss parent company has not been given up by the legislative change which entered into force on 1 April 2017. However, the flexibility introduced with the new rules regarding intra-year on-lending as well as the new safe harbor rule is highly welcome.

Stefan Oesterhelt (stefan.oesterhelt@homburger.ch)