New rules for digital assets have been proposed by the Federal Council in its Dispatch to the Parliament of 27 November 2019 in Switzerland. This contribution provides a brief overview of the big picture, the key legal amendments related to distributed ledger technology, as well as the latest adjustments to the draft of the DLT-Rules of 27 November 2019 in comparison to the Preliminary Draft of 22 March 2019. Further, the impact of the new rules on market participants is discussed.

By Luca Bianchi (Reference: CapLaw-2020-01)

1) Introduction

Great news for the digital assets industry: the Federal Council has adopted and submitted the Dispatch of 27 November 2019 on the Federal Act on the Adaptation of Federal Law to Developments in Technology of Distributed Ledgers (the Dispatch) to the Parliament. The proposed new rules for digital assets aim to further improve the framework conditions for distributed ledger technology (DLT) in Switzerland. The latest draft of the DLT-Rules of 27 November 2019 (the DLT-Rules) is the result of a collective effort of the federal administration, market players, industry associations, and other participants of the consultation proceeding (which ended on 28 June 2019) regarding the Preliminary Consultation Draft of the DLT-Rules of 22 March 2019 (the Preliminary Draft). Now, the Parliament has a chance to discuss the DLT-Rules (which already comprise the results of the consultation process).

This contribution serves as a general introduction to this CapLaw edition (which is dedicated to the DLT-Rules). More detailed reflections on the key areas and latest developments of the DLT-Rules are provided in the other articles of this newsletter. Notably, various updates on related developments have already been provided over the last years (see CapLaw 2019-15, 2017-02, 2016-47, and 2016-31). The contribution at hand builds on these foundations and contains selected repetitions thereof.

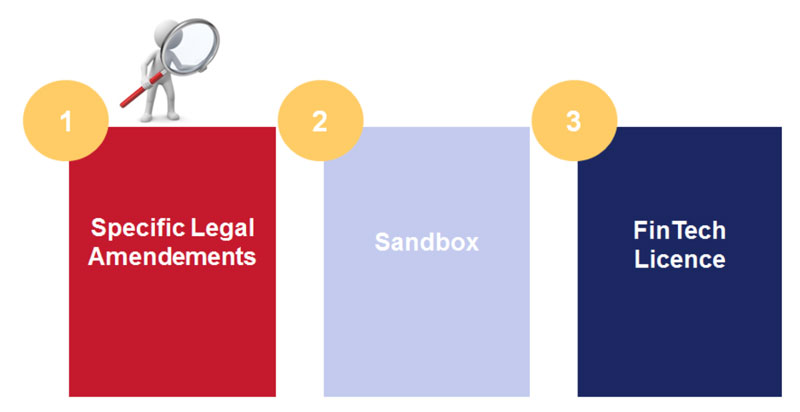

2) The Big Picture: Three Element Approach of Swiss FinTech Regulation

The regulation of Financial Technologies (FinTech) has become a new chapter of financial market law in Switzerland as well as worldwide. In this context, the Federal Council and the Federal Department of Finance (FDF) have developed a model for a Swiss FinTech (de)regulation, namely, the “Three Element Approach” set out in the following graph:

(See CapLaw 2017-02, p. 14, with further references)

As indicated in the above graph, the existing regulatory mismatch between historically grown and, thus, outdated laws and new business models shall be (further) reduced by three different elements. This CapLaw edition takes a closer look on the next milestone in terms of specific legal amendments (Element 1) – the DLT-Rules. The DLT-Rules are a logical consequence of the FinTech strategy of the Swiss authorities.

3) New Rules for Digital Assets

a) Specific Legal Amendments in Key Areas

Specific legal amendments for digital assets are proposed in the following key areas:

(See CapLaw 2019-15, p. 22)

The key legal areas of the DLT-Rules have already been discussed in a tour d’horizon provided by the author in CapLaw-2019-15 (based on the Preliminary Draft). Thus, only selected adjustments made in the latest draft of the DLT-Rules shall be elaborated in the following section 3)b). However, a closer look at the inner mechanics of the DLT-Rules can be found in the other contributions of the present CapLaw edition.

b) Selected Adjustments based on the Dispatch of the Federal Council

vis-à-vis the Preliminary Draft

The draft of the DLT-Rules of 27 November 2019 contains the following selected adjustments when compared to the Preliminary Draft of 22 March 2019:

– Civil Law: A new registered DLT-Uncertificated Security (i.e., a right which is entered in a register of uncertificated securities (Wertrechte)) (DLT-Uncertificated Securities) is being introduced in securities law (article 973d of the Swiss Code of Obligations (CO)). The transfer of DLT-Uncertificated Securities shall be subject to the rules of the registration agreement (article 973f(1) D-CO). Furthermore, it is interesting to note that a provision limiting bearer shares to listed companies and companies with shares that represent intermediated securities (Bucheffekten) in terms of the Federal Intermediated Securities Act (FISA), which are deposited with a custodian in Switzerland or stated in the main register has been inserted in the DLT-Rules (article 622(1bis) D-CO). However, this provision has already entered into force on 1 November 2019 and reflects a mere cosmetic adjustment in the context of the DLT-Rules.

– Insolvency Law: The bankruptcy administration shall explicitly be able to issue a decision on the release of crypto-based assets over which a joint debtor has the power of disposal at the time of the opening of bankruptcy proceedings and which are claimed by a third party (article 242a(1) D-DEBA). Such claim shall be deemed to be well-founded if the joint debtor has committed itself to hold the crypto-based assets ready for the third party at any time and these are either (i) individually assigned to the third party, or (ii) assigned to a community and it is clear what proportion of the joint assets belongs to the third party (article 242a(2)(a-b) D-DEBA).

– International Private Law: A revised article 106(2) D-PILA has been proposed which states that if a physical title represents goods the rights in rem (dingliche Rechte) to the title and to the goods shall be subject to the law applicable to the title as a movable object.

– Financial Market Law: The legal definition of the term securities (Effekten) shall be adjusted in the Financial Services Act (FinSA) and the Financial Market Infrastructure Act (FMIA). “Securities” comprise standardized securities suitable for mass trading, uncertificated securities (Wertrechte), in particular, simple uncertificated securities pursuant to article 973c D-CO and registered DLT-Uncertificated Securities according to article 973d D-CO, as well as derivatives and intermediated securities (Bucheffekten) (article 3(b) D-FinSA; article 2(b) FMIA). Furthermore, article 2(bbis) FMIA shall set out the (revised) definition of DLT-Securities (DLT-Effekten) which now explicitly comprises DLT-Uncertificated Securities according to article 973d D-CO as well as other uncertificated securities held in distributed electronic registers which, by means of technical procedures, give the creditors, but not the debtor, the power to dispose of the uncertificated securities. Moreover, a new definition of the term DLT-trading system has been proposed in article 73a D-FMIA.

Besides, various new provisions have been suggested to the Federal Intermediated Securities Act (FISA). In particular, DLT-Uncertificated Securities are newly listed in the catalogue of feasible underlyings for the creation of intermediated securities (article 6(1)(d) D-FISA). However, it is required that DLT-Uncertificated Securities are decommissioned in the register of DLT-Uncertificated Securities they derive from (Dispatch, p. 76). Such amendments facilitate a conversion of DLT-Uncertificated Securities (according to article 973d D-CO) into intermediated securities (pursuant to article 3 FISA in connection with article 6(1)(d) D-FISA). These regulatory developments are in line with the ongoing market trend of a convergence of financial products.

In addition, the provisions of the Banking Act (BA) shall apply by analogy to persons, who are mainly active in the financial sector and: (i) commercially accept retail deposits of up to CHF 100 million or crypto-based assets designated by the Federal Council, or publicly advertise as doing so; as well as (ii) neither invest nor pay interest on these deposits or assets (article 1b(1)(a-b) D-BA). Crypto-based deposits from the public or crypto-based assets designated by the Federal Council held by persons referred to in article 1b(1) D-BA shall not be subject to the provisions on privileged deposits (article 37a BA) and on immediate payouts (article 37b D-BA); depositors must be informed of this fact before they make the deposit (article 1b(4)(d) D-BA). However, the term deposited assets according to article 37d D-BA (segregation of assets) includes crypto-based assets (article 16(1bis) D-BA). As a result, crypto-based assets in deposits shall be segregated pursuant to articles 17 et seq. FISA in case of a default (article 37d D-BA).

– Anti-Money Laundering Regulations: In the Anti-Money Laundering Act (AMLA), article 2(2)(dbis-dter) D-AMLA shall be adjusted in order to comply with the DLT-Rules (in particular, the provisions of the D-FMIA). Further, a number of rather technical adjustments to the AMLA have been proposed.

4) Impact on Market Participants

a) General Impact

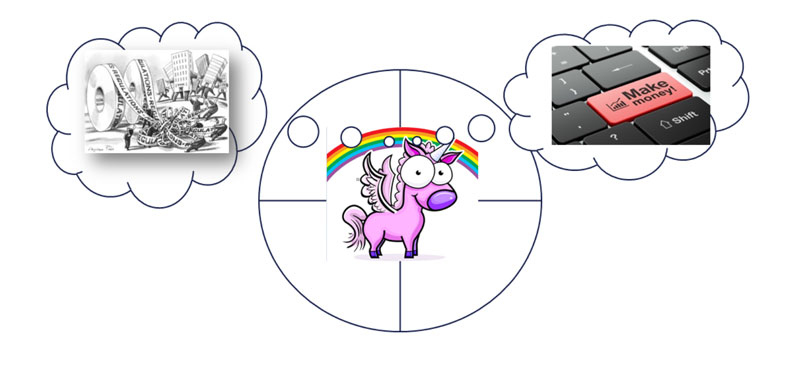

Innovative market participants in the area of digital assets currently face the challenge of evaluating the impact of the new Swiss financial market architecture. In particular, the FinSA as well as the FinIA have entered into effect on 1 January 2020 and are currently being implemented. At the same time, market participants have to follow the legal developments regarding digital assets. However, the DLT-Rules will, hopefully, allow them to see the light at the end of the (regulation) tunnel in terms of finally being subject to a punctual deregulation after a decade of ever increasing financial services and products regulation.

Against this background, the following chart illustrates the innovative digital assets company (symbolized by the pink unicorn) which will have to keep one eye on the new financial market architecture (compliance) and the other eye on the DLT-Rules (which rather represent a business opportunity):

b) Impact on Business Areas

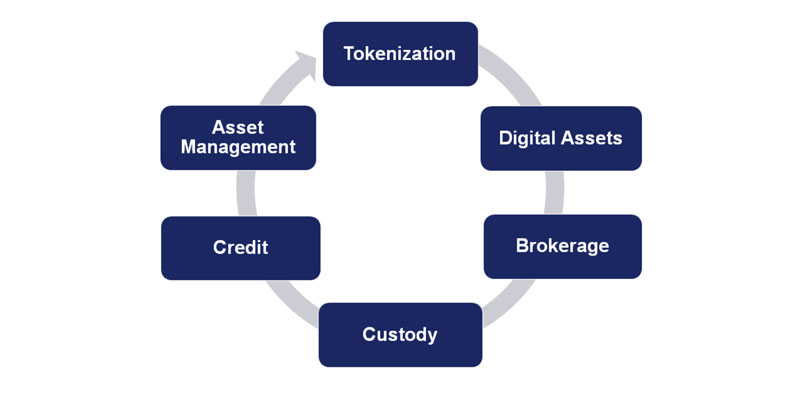

The DLT-Rules will affect different business areas in the value chain of the digital assets industry:

Market participants must evaluate if and to what extent their business will benefit or be restricted by the DLT-Rules because once the proposal is final and enters into effect it will have to be implemented in internal guidelines and policies, in the product documentation, as well as regarding operative processes. Regulatory licenses or approvals may have to be obtained (where required by financial market law).

5) Conclusion

The DLT-Rules are a fast and appropriate reaction of the Federal Council and the FDF to the ICO-boom of 2014-2018. Further, the general design of the proposed regulation shows the openness of the Swiss authorities towards innovation as well as the ongoing trend of a convergence of financial products. In addition, the increase of legal certainty regarding the transfer of digital assets provided by the DLT-Rules is very welcome and allows digital asset providers to create better products. However, the DLT-Rules will have a major impact on the new kids on the block in the financial services and products industry (i.e., challenger banks and other innovative companies in the digital assets industry). Thus, it will be interesting to see how the Parliament will further deal with the DLT-Rules.

Luca Bianchi (luca.bianchi@nkf.ch)