On 3 April 2020, the Swiss Federal Council opened the consultation procedure for the new proposal to reform the Swiss withholding tax system and the proposal to abolish the transfer stamp duty on trading in certain securities. The consultation period ended on 10 July 2020. The present article provides for an overview over these proposals.

By Stefan Oesterhelt (Reference: CapLaw-2020-41)

1) Current situation

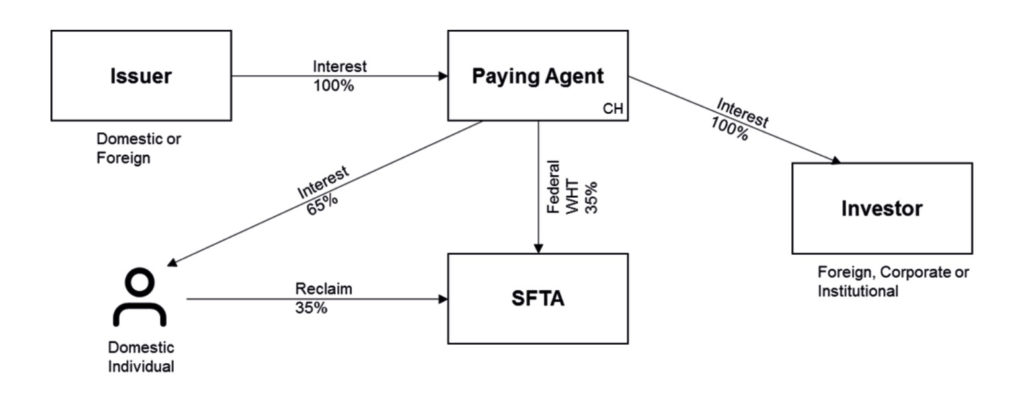

While interest payments on single loans are not subject to withholding tax in Switzerland, interest payments on bonds of a domestic issuer are subject to Swiss Federal Withholding Tax of 35 percent. Swiss bonds are therefore particularly unattractive for foreign investors, even if they are entitled to a partial or full tax refund based on a double taxation treaty (specifically, investors resident in Austria, Denmark, Czech Republic, Finland, France, Germany, Ireland, Iceland, Liechtenstein, Luxemburg, Norway, UK and the US, amongst others, are entitled to a full refund.).

The reasons for this are the liquidity disadvantage between levying and refunding the withholding tax and the administrative costs associated with the refund. In response, Swiss groups regularly avoid withholding tax by issuing their bonds through a foreign company. The Swiss Federal Tax Administration introduced new rules recently to give more flexibility regarding the potential on-lending into Switzerland of such issuances (see Stefan Oesterhelt, Swiss Debt Capital Markets: More Flexibility under New Swiss Withholding Tax Rules, CapLaw-2019-44).

Furthermore, transfer stamp duty is levied on trading in certain securities, including bonds. The tax is payable if at least one of the parties involved in trading is a Swiss securities dealer. Half the tax is payable per securities dealer involved. The total levy for domestic bonds is 0.15 per cent of the sales proceeds, and 0.3 per cent for foreign securities. According to the proposal of the Federal Council of 3 April 2020 the transfer stamp duty would be abolished on domestic bonds (see below at 4)).

2) Reform efforts to date

a) Federal Council proposal 2010

The Federal Council had already launched a reform of the withholding tax in 2010 (for an overview of the 2010 proposal of the Federal Council, see Dieter Grünblatt and Stefan Oesterhelt, Swiss Capital Markets: Welcomed Fundamental Changes in Taxation of Debt Instruments Ahead, CapLaw 2011-42). The trigger for the bill at that time was the introduction of the TBTF instruments (i.e., AT1 issuances such as CoCo bonds and Write-down Bonds). However, Parliament rejected the proposal to the Federal Council. Instead, it decided to exempt these TBTF instruments from withholding tax (Federal Act of 15 June 2012). A few years later, TLAC issuances have been exempt from withholding tax as well (Federal Act of 18 March 2016).

b) Proposal of the Federal Council 2014

The Federal Council made a further attempt on 17 December 2014 for a reform of withholding tax on interest (for an overview of the 2014 proposal see Stefan Oesterhelt, Withholding Tax on Interest to be Replaced by Paying Agent Tax System, CapLaw 2015-5). The Federal Council’s reform proposal was based on a concept developed by the Brunetti group of experts. The Federal Council suspended the project in June 2015 in view of the controversial outcome of the consultation process and against the backdrop of the then pending popular initiative Ja zum Schutz der Privatsphäre, which wanted to anchor fiscal banking secrecy in the constitution. In November 2015, it instructed the Federal Finance Ministry to set up a group of experts to develop reform proposals. On this basis, the Federal Council wanted to decide on further action as quickly as possible after the vote on the popular initiative.

c) New Federal Council proposal

After the popular initiative was withdrawn in January 2018, the expert group intensified its work. It delivered its report at the end of 2018. The Federal Council was informed in March 2019. In addition to a reform in favor of the debt capital market, the group of experts also proposes examining measures for the equity capital market.

3) Withholding tax on bonds: transition to the paying agent principle

a) Principles

In order to abolish the disadvantage of domestic bond issues compared to foreign bond issues, the Federal Council proposes in its consultation draft of 3 April 2020 to switch to the paying agent principle for bond issues. Under the paying agent principle, the withholding tax is not paid by the debtor of the interest payment (e.g., a company that issues a bond and pays interest on it), but by the investor’s paying agent (e.g., the bank in whose custody account the investor holds the taxable bond).

Unlike the debtor, the paying agent knows the identity of the investor. It is therefore in a position to levy withholding tax only in those cases where this is required for security purposes, namely in relation to individuals resident in Switzerland. By contrast, domestic legal entities and foreign investors are exempt from the tax. Domestic banking secrecy for tax purposes remains intact. As is currently the case, the tax authorities will only learn of the existence of the income and assets subject to withholding tax at the time of the investor’s declaration.

b) Scope: interest payments on bonds

The paying agent principle only covers interest payments on bonds (Anleihensobligationen) and debentures (Kassenobligationen). Withholding tax on dividends is not levied based on the paying agent principle, but on the debtor principle. Interest payments on customer balances (Kundenguthaben) are also not covered by the paying agent principle.

However, interest payments on bonds of indirect investments (structured products and collective capital investments) are also covered by the paying agent principle (cf. section 3)f) below). In addition, interest payments on bonds of foreign issuers should also be subject to paying agent tax (see 3)d) below).

The proposal only covers Swiss Federal Withholding Tax. Withholding tax levied by the Cantons on bonds secured by Swiss real estate is not covered by the paying agent principle (for a detailed overview over this withholding tax see Stefan Oesterhelt and Maurus Winzap, Quellensteuern bei hypothekarisch gesicherten Kreditverträgen, FStR 2008, pp. 28.).

c) Paying agents covered

According to the proposal, withholding tax will always apply if the paying agent is domiciled in Switzerland, whereas in the case of the debtor principle the domicile of the debtor is decisive.

Banks are usually eligible as paying agents. However, if interest bearing securities are not held in a bank custody account (e.g., in the case of bonds issued by SMEs or corporate credit balances), the debtor of the taxable performance may also qualify as a paying agent. In this case, the debtor must identify its investors and is responsible for the correct payment of the new withholding tax.

d) Interest payments of foreign bond issuances

Furthermore, the paying agents are technically able to levy withholding tax on income from foreign interest securities. This means that foreign interest income is now also secured if it is held by a domestic individual in a securities account at a domestic bank. This is intended to close a significant security gap and contribute to combating tax evasion.

However, the recording of interest payments from foreign issuers always leads to considerable practical difficulties when it comes to combined products (such as convertible bonds or structured products) that are not included in the list of securities of the FTA (or a comparable new database to be created).

e) Optional continued application of the debtor principle

Under the new proposal, the domestic debtor would have the possibility to choose whether to apply the debtor principle (as today) or the paying agent principle. If he opts for the debtor principle, he will, as today, pay the withholding tax for all investors. Domestic SMEs and collective capital investments can, thus, be exempted from the additional obligations that the new withholding system entails.

f) Scope of application for indirect investments

The paying agent principle applies to all interest income. It is intended to cover not only direct investments in interest-bearing securities, but also indirect investments via a collective investment scheme or a structured product. This applies to both distributed and reinvested interest income. However, dividend income and capital gains are not covered by the paying agent principle. Withholding tax is still levied on the former according to the debtor principle. The latter are tax-free.

g) Comparison with proposal 2014

In the consultation process, the 2014 proposal was rejected by the banks, in particular because they considered the administrative effort, costs, settlement and liability risks to be disproportionately high. The 2020 proposal is intended to take some of these considerations into account:

i. Limitation of the paying agent principle to interest income only. (In its 2014 proposal, the Federal Council had also proposed that foreign dividend income should be included).

ii. The criminal liability of paying agents is excluded in cases of negligence.

iii. The 2020 proposal contains an option for the debtor principle, which is particularly beneficial to SMEs.

iv. Restriction of withholding tax to domestic individuals.

v. No recording of accrued interest.

vi. Quarterly delivery of the withholding tax.

Nevertheless, the 2020 proposal is still quite complex and therefore subject to criticism, especially by the banks (see Petrit Ismajli and Urs Kapalle, Geplante Reform der Verrechnungssteuer, EF 2019, pp. 894; Stefan Keglmaier and Charles Hermann, Une occasion manquée, EF 2020, pp. 513).

h) Further legislative process

The Federal Council opened the consultation procedure for the new proposal on 3 April 2020. The consultation period ended on 10 July 2020. Most participants in the consultation process acknowledge the need for action. However, the proposal is still considered too burdensome to implement for the paying agents, which is why the Federal Council will once again thoroughly revise the proposal before issuing a dispatch. It is expected to be able to be discussed in parliament in 2021. The earliest possible date for the revision to enter into force would be 2022, but this date is unrealistic. Therefore, it is not expected to enter into force before 2023. Furthermore, it is expected that the paying agents will be granted a transitional period to make the necessary preparatory steps to introduce such a paying agent system (Fabian Baumer, Reform der Verrechnungssteuer – ein Projekt zur Unzeit?, StR 2020, pp. 118, 124).

4) Abolition of the turnover tax on domestic bonds

Trading in domestic bonds is currently subject to a 0.15% turnover tax. To further strengthen the domestic capital market, the turnover tax on trading in domestic bonds is to be abolished. However, trading in foreign bonds will remain subject to the 0.3% turnover tax.

In contrast to the relatively complex introduction of a paying agent principle for interest payments, the abolition of the turnover tax on domestic bonds could be introduced relatively easily. Implementation in the course of 2021 would theoretically be possible. Without the introduction of the paying agent principle, however, the abolition of the turnover tax on domestic bonds would do little to significantly strengthen Swiss bond issuances.

Stefan Oesterhelt (stefan.oesterhelt@homburger.ch)