On 21 October 2020, the Swiss Federal Council published a message to Parliament (Botschaft) (message-ISA) for a revision of the Insurance Supervision Act (ISA), including a draft of the new provisions (draft-ISA). Among others, the proposed legislation introduces new rules regarding the distribution of insurance products (point of sale), in particular insurance products with investment character (qualified life insurance products), and thereby to some extent aligns the distribution rules with those of the Swiss Financial Services Act (FSA). In addition, the proposed new rules provide for certain far-reaching changes for insurance intermediaries, which affect the scope of their services, their organization and cooperations.

By Bertrand Schott / Simon Bühler (Reference: CapLaw-2020-71)

1) Overview

The proposed new regulation concerning obligations at the point of sale leads to a certain alignment with the FSA, in particular with regard to the new category of qualified life insurance products. Insurance products are outside the scope of the FSA. The aim of the new regulation is to create a level playing field among investment instruments, which made it necessary to create a regulation similar to the FSA for insurance products that have an investment character.

In our view, the new duties of the draft-ISA are of purely supervisory law nature, i.e. they are in particular not provisions of civil law or of a dual nature (Doppelnormen). Further, one should also note that the revision of the Swiss Insurance Contract Act (coming into force on 1 January 2022) further increases the protection of the insureds.

The regulation in the draft-ISA is designed to cover distribution activities, in particular the recommendation of products, rather than for example portfolio-related advice or portfolio management, which is why, for example, the draft-ISA does not provide for a duty to perform a suitability check as contained in the FSA. The new obligations at the point of sale apply in relation to all insureds; there is no client segmentation and corresponding gradation of point of sale obligations as provided for in the FSA. While the draft-ISA provides for a category of “professional insureds” as defined in the new Swiss Insurance Contract Act, these by their nature typically do not hold life insurance policies and, therefore, are usually outside the scope of most of the new distribution rules.

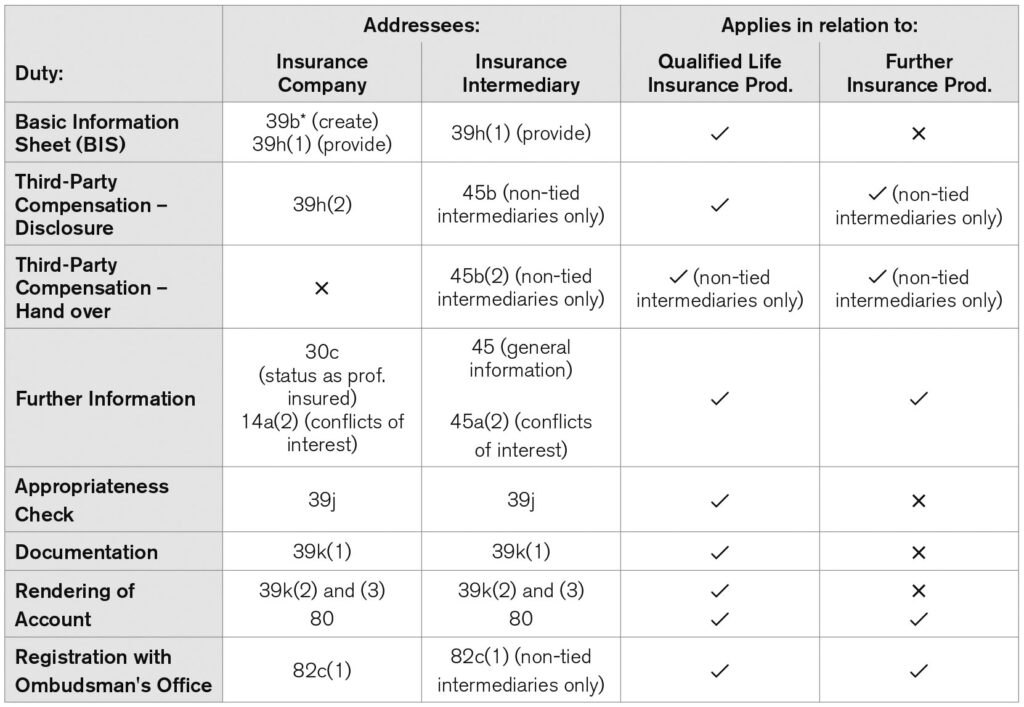

The following is an overview of the proposed point of sale obligations:

The draft-ISA also provides for certain other far-reaching changes for insurance intermediaries, which affect the scope of their services and their organization in relation to all insurance products. An important change concerns the new rule that insurance intermediaries may only be either tied or non-tied; both at the same time is no longer possible. This will require major business adjustments, including the review of existing cooperation agreements and joint ventures. There is still a registration requirement for non-tied insurance intermediaries, which has been extended and adapted to the FSA. Unlike under the FSA, one of the new draft-ISA requirements for entry in the register is that the non-tied insurance intermediary must have its seat, domicile or a branch in Switzerland (however, the Swiss Financial Market Supervisory Authority (FINMA) may grant exceptions in justified cases). Since the register for non-tied insurance intermediaries is kept directly by FINMA (unlike the adviser’s register under the FSA), non-tied intermediaries are supervised persons in the sense of the Swiss Financial Market Supervision Act. In contrast, tied insurance intermediaries are not subject to a registration requirement because they are already supervised by FINMA via the insurance company for which they work (unchanged).

The revised ISA is expected to enter into force no earlier than January 2022 with transitional periods for certain key changes, such as a transitional period of one year for the distribution rules regarding qualified life insurance products (for more details, see article 90a draft-ISA).

2) Proposed New Distribution Rules for Insurance Companies

and Intermediaries

a) Definition of Qualified Life Insurance Products

The proposed new rules at the point of sale mainly apply to so-called qualified insurance products (qualifizierte Lebensversicherungen; article 39a draft-ISA). As the message-ISA explains, this term is supposed to capture all insurance products with an investment character rather than pure risk insurance products.

Article 39a draft-ISA defines qualified life insurance products as (a) life insurance products that involve a risk of loss for the insured in the savings process, (b) capital redemption operations (Kapitalisationsgeschäfte) or (c) tontines (Tontinengeschäfte):

– Life insurance products that involve a risk of loss for the insured in the savings process concern products of all life insurance classes (except for classes A6 and A7 described below) that involve a risk of loss due to market fluctuations. As per the message-ISA, a risk of loss means that the present value of the savings portion of an insurance policy at the time of ordinary payment or conversion may be lower than the nominal amount of all savings premiums paid. Thus, life insurance products without investment components or with participation in surplus as the only investment component are not considered qualified life insurance products.

– Capital redemption operations (insurance class A6) are contracts under which the client transfers assets and delegates their management (based on a mathematical model) to an insurance company that involves no (or very limited) biometric risks (see FINMA circular 2016/6 “Life Insurance”, N 11). The message-ISA states that capital redemption operations, “as a rule”, involve an investment risk for the insured, which is why it is justified to classify them as qualified life insurance products.

– Tontines (insurance class A7) are contracts under which the contributions of all insureds are pooled and invested, whereby the investment risk remains with the insureds. The resulting capital is distributed as an annuity (lebenslange Rente) to the insureds alive and, if provided so in the contract, to the heirs of the deceased insureds (see message-ISA). In the words of the message-ISA, the “predominant capital market element” of tontines justifies treating them as qualified life insurance products.

The first category (life insurance products involving a risk of loss) was still referred to in the preliminary draft as “life insurance products involving an investment risk”, which is more far-reaching, because an investment risk can also consist of a product performing below average in comparison with other (comparable) products, for example. Under the proposed new rule (and according to the message-ISA), all life insurance products with capital protection (in the sense of protection of the investment brought in) are outside the scope of the definition.

b) Basic Information Sheet / Advertising

Insurance companies offering qualified life insurance products must prepare a Basic Information Sheet (BIS) (Basisinformationsblatt) for these with information that is easily understandable, kept up-to-date and enabling the insured to compare similar qualified life insurance products (article 39b-d draft-ISA; the FSA contains corresponding requirements). Article 39g draft-ISA introduces a liability for anyone who fails to exercise due care and thereby provides in the BIS information that is inaccurate, misleading or in violation of statutory requirements. When recommending a qualified life insurance product, the BIS must be provided (free of charge) by the insurance company or intermediary, respectively, prior to the conclusion of the contract (article 39h(1) draft-ISA).

Advertisements for qualified life insurance products must be clearly recognizable as such (article 39i(1) draft-ISA). The advertisement must contain a reference to the BIS and to where it can be obtained (article 39i(2) draft-ISA). Information conveyed (by advertising or other means) must be consistent with the information in the BIS (article 39i(3) draft-ISA).

c) Duty to Provide Information

As is already the case under current law, insurance intermediaries will be subject to a duty to provide certain basic information to their clients in advance in relation to all insurance products (for details, see article 45 draft-ISA that extends the scope of information to be provided). The information may be provided electronically and in standardized form. Specific information duties apply with regard to compensation from third parties (see 2) f)) and potential conflicts of interest (see 3) c)).

d) Appropriateness Check

Before providing recommendations on qualified life insurance products, the insurance company or intermediary, respectively, has to perform an appropriateness check (article 39j draft-ISA; the FSA contains a corresponding requirement). To this end, the insurance company or intermediary, respectively, must request information on the insured’s knowledge and experience. If the insurance company or intermediary, respectively, concludes that a qualified life insurance product is not appropriate for the insured, it shall advise the insured against such product. If the information provided is not sufficient to assess appropriateness, the insured must be informed that no appropriateness check is conducted.

No appropriateness check is required if a qualified insurance product is concluded on the initiative of the insured and without rendering personal advice (execution only).

e) Documentation and Rendering of Account

Insurance companies and intermediaries shall be subject to documentation and accountability obligations for qualified life insurance products under the proposed new rules (article 39k draft-ISA). The documentation requirement includes (a) the keeping of record of which qualified life insurance contract was concluded, (b) the information collected on knowledge and experience of the insureds, (c) the absence of an appropriateness test (if applicable) and (d) any issued recommendation against entering into qualified life insurance contracts.

On request, insurance companies and intermediaries shall be required to provide the insureds with (a) a copy of the documentation (or make it available in another appropriate manner) and (b) information on the underlying financial instruments’ valuation, performance and costs. The insureds’ entitlement and the procedure for obtaining a copy of the file and other information is governed by articles 80 et seq. draft-ISA.

f) Compensation from Third Parties

Compensation from third parties regularly aim at promoting certain types of insurance products and thus lead to a potential conflict of interest for the party distributing the insurance products. The draft-ISA addresses this as follows:

Insurance companies are required to inform insureds about compensation from third parties received in connection with qualified life insurance products when recommending such products (article 39h(2) draft-ISA), but not about compensation paid to insurance intermediaries (see message-ISA). Neither the draft-ISA nor message-ISA yet define the type and scope of information required. In our view, the standard as set forth for non-tied insurance intermediaries (see below) may be applied.

Non-tied insurance intermediaries are by definition in a fiduciary relationship (Treueverhältnis) with the insureds and must act in their interest (as opposed to tied insurance intermediaries who typically act on behalf of an insurance company). The proposed new regulation contains the following rules that apply in relation to all insurance products intermediated (article 45b draft-ISA):

– In case remuneration of the non-tied insurance intermediary is limited to commissions received from insurance companies (or from any third party): If the non-tied insurance intermediary receives its entire compensation from the insurance company or from any third party (commission), there is a duty to inform the insured in advance of such commission (see below).

– In case remuneration of the non-tied insurance intermediary includes both commissions received from insurance companies (or from any third party) and (direct) compensation from the insured: If the non-tied insurance intermediary receives both a commission from the insurance company (or from any third party) and a remuneration from the insured at the point of sale, a disclosure of the commissions is not sufficient. In addition, the insurance intermediary must obtain from the insured an express waiver regarding the handing over of the commission. If no such waiver is obtained, the commissions must be handed over to the insured.

In both cases (as described above), the information regarding compensation from third parties must meet certain minimum requirements (article 45b(3) draft-ISA). In terms of content, it must include the type and scope of the remuneration. Disclosure of calculation parameters and bandwidths is sufficient if the amount is not determinable in advance (i.e., prior to the conclusion of the contract between the non-tied intermediary and its client). If, in such cases, calculation parameters and bandwidths are disclosed in advance, this is sufficient in our view, i.e. the non-tied intermediary does not need to provide further information on the individual (concrete) third-party compensation at a later date when the amount of such third-party compensation can be determined. Further, the information must be provided in advance, i.e. “before the service is provided or before the contract is concluded”. In addition, the non-tied insurance intermediary must provide information on actual compensation received from third parties on request.

Compensation in the above sense is defined as payments from third parties accruing to the non-tied insurance intermediary in connection with the provision of a service, such as brokerage fees, commissions, discounts or other financial benefits (article 45b(4) draft-ISA; the FSA contains a corresponding definition).

3) Proposed New Rules for Insurance Intermediaries

a) Obligation to Opt for either Tied or Non-Tied Intermediary

Against the background of protecting insureds from conflicts of interest, the proposed new regulation prohibits insurance intermediaries from operating as tied (on behalf of an insurance company) and non-tied (in the interest of the insured) insurance intermediary at the same time (article 44(1)(b) draft-ISA).

The clear distinction between tied and non-tied intermediaries is also the basis for a more focused supervision by FINMA; FINMA has signaled that it will expand its supervision of non-tied intermediaries (see message-ISA and article 46 draft-ISA concerning FINMA’s tasks).

b) Registration

Non-tied insurance intermediaries may carry out their activity only if they are entered into a register of non-tied insurance intermediaries that is kept by FINMA (articles 41(1) and 42 draft-ISA). The draft-ISA plans to expand the current registration requirements by introducing the requirements of (a) seat, domicile or branch in Switzerland, (b) good reputation and the guarantee for the fulfillment of obligations under the draft-ISA, and (c) registration with an ombudsman’s office (article 41(2) draft-ISA).

The proposed introduction of a new requirement to have a seat, domicile or branch in Switzerland means that foreign non-tied insurance intermediaries without physical presence in Switzerland (i.e. acting on a pure cross-border basis) would no longer be admissible for registration and thus for carrying out their activity in Switzerland (in contrast to foreign “advisers” under the FSA). Only activities outside the territorial or substantive scope of the draft-ISA would remain permissible (e.g. see article 2(2)(f) draft-ISA concerning the intermediation of certain supplementary insurance products). The message-ISA explains that this requirement “appears to be essential for effective supervision by FINMA”, in particular the enforcement of its supervisory instruments. However, FINMA may grant exceptions in justified cases (begründeten Fällen). The message-ISA does not specify what such cases may be.

Tied insurance intermediaries are not subject to registration duties. In contrast to today, they may no longer register themselves voluntarily, unless they provide evidence of desiring to take up an activity abroad and of the foreign law requiring a Swiss register entry (article 42(4) draft-ISA).

c) Conflicts of Interest / Organizational Precautions

Insurance intermediaries (tied and non-tied) are obliged to (a) identify potential conflicts of interest and (b) take adequate organizational measures to prevent these from occurring or from disadvantaging the insureds (article 45a(1) draft-ISA). If disadvantages for insureds cannot be excluded, this must be disclosed to them before concluding an insurance contract (article 45a(2) draft-ISA). The Federal Council is authorized to regulate the details. A corresponding obligation exists for insurance companies in article 14a draft-ISA.

d) Basic Training and Further Education

Insurance intermediaries (tied and non-tied) are required to have the skills and knowledge necessary for their activities (article 43 draft-ISA). The insurance companies and the insurance intermediaries have to define sector-specific minimum standards for basic training and further education. Should no appropriate minimum standards exist, the Federal Council shall determine these.

e) Ombudsman’s Office

Non-tied insurance intermediaries (as well as insurance companies) are required to register with an ombudsman’s office (article 82c(1) draft-ISA). This aims at providing insureds with the possibility of a mediation procedure before an ombudsman for all disputes (see message-ISA). The Swiss Federal Department of Finance is responsible for recognizing ombudsman’s offices; recognition is subject to certain requirements being met (article 83 draft-ISA). Insurance companies that have only professional insureds may on request be exempt from a registration with an ombudsman’s office.

Bertrand Schott (bertrand.schott@nkf.ch)

Simon Bühler (simon.buehler@nkf.ch)