The financial sector plays an important role in addressing climate change issues. While it is recognized that climate change can have an impact on financial stability, the financial sector can contribute to a reduction in greenhouse gas emissions. This article provides an overview of the various green / sustainable financing methods and their main characteristics, and summarizes recent developments in financial law and regulation to strengthen credibility of and faith in sustainable financial products.

By Charlotte Rüegg (Reference: CapLaw-2020-15)

1) Introduction

In connection with the 2015 Paris Climate Convention, Switzerland has committed to reduce its greenhouse gas emissions by 50 per cent. until 2030 (compared with the greenhouse gas level in 1990).

Due to increased climate awareness following climate strikes (#WeekForClimate) all over the world with more than 6 million participants, governments and companies alike have revised and tightened their climate goals. By way of examples, Amazon committed itself to climate-neutrality by 2040 and Microsoft made a pledge to be carbon negative by 2030. The revised goal defined by the Federal Council is to achieve CO2 neutrality by 2050. This means that from 2050 onwards Switzerland’s CO2 emissions shall not be greater than what can be absorbed by way of natural (e.g. conversion of CO2 to O2 by plants) or technical means (e.g. equipment that removes CO2 from the atmosphere).

Pursuant to OECD’s estimates, sustainable investments in the amount of USD 7 trillion are required by 2030 in order to achieve these goals. Such amounts can be absorbed by the loan, bond and other securities markets around the world. In addition, it is important that governments and regulators define and implement uniform rules to encourage and support green and sustainable investments and to avoid greenwashing (greenwashing is considered to give a false impression or misleading information about how a company’s products / services are more environmentally sound).

2) Green, Social and Sustainable Finance – an Overview

Since 2007, when the European Investment Bank issued the first green bond, a lot has been done to move the needle towards green and sustainable finance. Regulators and governments like the EU Technical Expert Group and industry players like ICMA, LMA or rating agencies have introduced principles and guidelines to provide transparency and promote investments in the green loan / bond market.

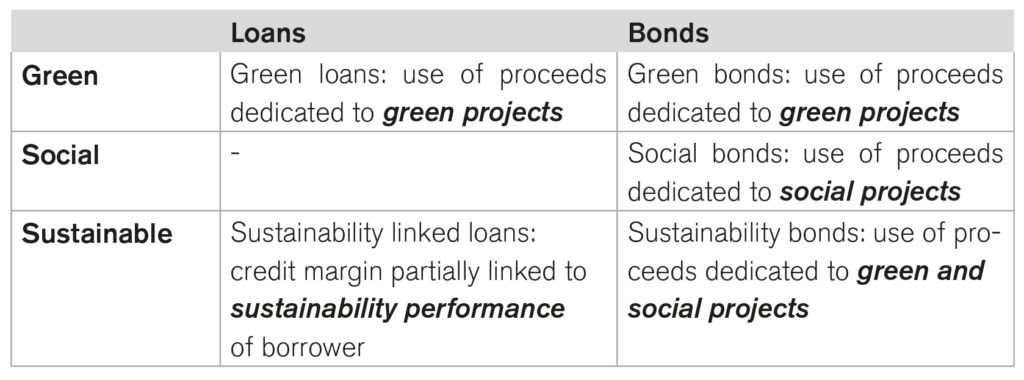

The below table provides a high-level overview of the terminology and the major characteristics of the various loan and bond types, as such terms are currently used:

That said, there are no standard definitions of the terms “Green Finance” and “Sustainable Finance”. In the following paragraphs, reference is made to the respective definitions provided by the Loan Market Association (LMA) and the International Capital Markets Association (ICMA).

a) Green, Social or Sustainability Bonds

“Green / social bonds are any type of bond instrument where the proceeds will be exclusively applied to finance or re-finance new and/or existing eligible green / social projects and which are aligned with the four core components of the ICMA Green Bond Principles (“GBP”) / ICMA Social Bond Principles (“SBP”).”

As any type of bond instrument can serve as a basis for a green / social bond there are no limits in structuring a green / social bond issuance. The GBPs and the SBPs list four types of bonds (i.e. plain vanilla bonds, revenue bonds, project bonds or bonds in connection with a securitization) and point out that depending on market developments additional types of bonds may fulfil the eligibility criteria to serve as basis for a green / social bond issuance.

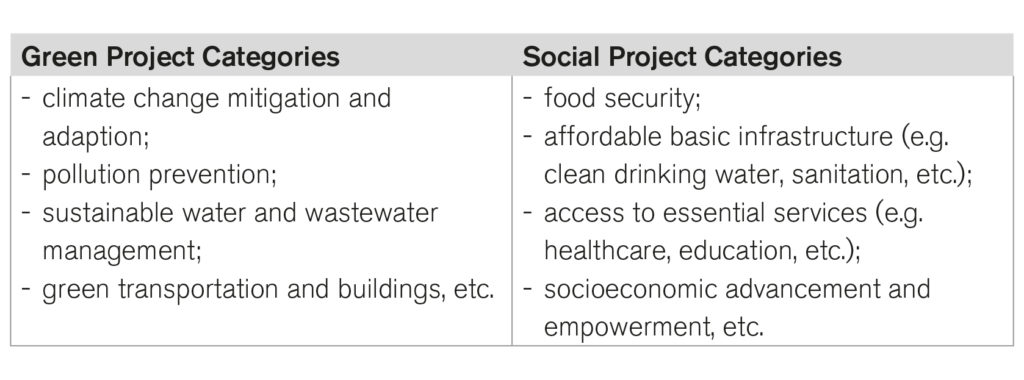

Further, the proceeds from green / social bond issuances may be used for new financing or re-financing purposes, provided that the use of proceeds is in line with the principles. Both the GBPs and the SBPs include non-exhaustive lists with green / social project categories such as:

The four core components of the GBPs / SBPs are as follows:

– use of proceeds (i.e., determination of utilization and description of contribution to environmental goals like climate change mitigation / adaption, natural resource / biodiversity conservation, pollution prevention or green buildings / infrastructure);

– process for project evaluation and selection (i.e., disclosure of process / criteria to determine green / social projects and to identify / manage environmental and social risks associated with the project);

– management of proceeds (i.e., tracking and ringfencing of proceeds to be used for green / social projects to meet high transparency requirements); and

– reporting (i.e., annual report contains description of green / social projects and allocation of proceeds whereas material developments have to be reported on an ad hoc basis).

Sustainability bonds are a combination of the above-mentioned green and social bonds. That said, the proceeds of sustainability bonds are exclusively applied to finance or re-finance a combination of both green and social projects, all in compliance with the four core components of both the GBPs and the SBPs.

b) Green Loans

“Green loans are any type of loan instrument made available exclusively to finance or re-finance new and/or existing eligible green projects and which are aligned with the four core components of the LMA Green Loan Principles (“GLPs”).”

Pursuant to the LMA definition any type of facility can meet the eligibility criteria to qualify as green loan, i.e. no matter whether it is a term loan or a revolving credit facility. The latter comes with higher monitoring costs as to the use of proceeds and the identification of the “green” use of proceeds may not be as crystal clear as with respect to a term loan.

The other components of the definition of green loans are the same as with respect to green / social bonds. This is due to the fact that the LMA Green Loan Principles are based on the GBPs and quite similar.

c) Sustainability Linked Loans

“Sustainability Linked Loans are any type of loan instruments and / or contingent facilities (such as bonding lines, guarantee lines or letters of credit) which incentivize the borrower’s achievement of ambitious, predetermined sustainability performance objectives (LMA Sustainability Linked Loan Principles, “SLLPs“).”

Same as the GBPs and the GLPs, the SLLPs have four core components:

– link to borrower’s overall corporate social responsibility strategy (i.e., clear communication by borrower to lenders of sustainability objectives and how these align with sustainability performance targets);

– target setting – measuring the sustainability of the borrower (i.e., negotiation between borrower and lenders of appropriate sustainability performance targets with a view to incentivize improvements in borrower’s sustainability profile over the term of the loan);

– reporting (i.e., provision of information relating to borrower’s sustainability performance and indicators to lenders on a regular basis); and

– review (i.e., need for external review (e.g. by an auditor, environmental consultant, ratings agency) to be negotiated and agreed between borrower and lenders (for publicly traded companies reliance on borrower’s public disclosures may be sufficient for lenders to verify borrower’s performance against the sustainability performance targets)).

The key difference between sustainable loans and green loans is that the proceeds borrowed under a sustainable loan are not tied to a green project, rather the proceeds may be used for general corporate purposes, refinancing of existing financial indebtedness, acquisitions, etc. That said, the sustainability factor is not linked to the use of proceeds but to the sustainable performance of the borrower and there is a financial incentive if the borrower improves on the relevant sustainability criteria. Therefore, the sustainability linked loan market is open to all sizes of corporates, in particular, also small and medium sized companies which cannot come up with a project which requires ESG (environmental, social and governance) funding.

By way of illustration, the sustainability link can be described by the “carrot and stick” model, where the borrower receives a discount if it meets the defined performance targets (carrot) and needs to pay a premium if it fails to meet the required targets (stick). Therefore, it is required that the borrower and the lenders agree on the mechanics of the sustainability linked loan documentation. There are various options how a sustainability linked loan can be structured, e.g. by way of the following mechanics:

– margin ratchets: margin in- or decreases depending on whether the borrower meets predefined ESG goals (e.g. 50% reduction in printing operations / greenhouse gas emissions / air travels etc. over 5 years);

– ratings linked financing costs: margin linked to company’s sustainability rating provided by sustainability rating agency; or

– KPIs linked benchmark: margin linked to defined KPIs published by the borrower.

A failure by a borrower to meet its sustainability goals does not trigger any prepayment events or events of default. Rather, it results in an increase of the financing costs.

d) Collateralized Loan Obligations

Sustainability linked loans have, in addition to the flexible use of proceeds, another beneficial feature in that they serve as ideal collateral for sustainable securitizations. Such instruments are essential to provide investment opportunities to a vast range of investors and to connect institutional investors’ capital in the bond market with sustainable investments on the loan market level.

This is where monitoring, reporting and disclosure obligations become even more important so that investors have comfort that the underlying assets meet and continue to meet minimum ESG requirements.

3) Legal and Regulatory Developments and Achievements

“To bring climate risks and resilience into the heart of financial decision-making, climate disclosure must become comprehensive, climate risk must be transformed, and investing for a two-degree world must go mainstream” Mark Carney, Governor of the Bank of England (2013-2020), during speech given at the Task Force on Climate-related Financial Disclosure Summit on October 8, 2019 in Tokyo.

Sustainability-related disclosure requirements are necessary and a standardized taxonomy is key to encourage sustainable investments – whether effected by way of legislative acts and regulatory requirements or by way of rules or guidelines of self-regulatory organizations.

a) Switzerland

While the Swiss legislator is discussing a revision of the Reduction of CO2 Emissions Act (“CO2 Act“) to, inter alia, implement the greenhouse gas reduction commitments under the Paris Convention into Swiss legislation, it is not currently envisaged to integrate any sustainability-related disclosures in the financial sector and regulations for climate compatible investments into the CO2 Act. If and when any such provisions are implemented into Swiss legislation, they would likely be integrated into the special financial market laws acts, such as the Financial Markets Infrastructure Act or the Banking Act.

Under current Swiss financial market laws, there is no explicit obligation for financial institutions to consider climate risks and impacts in their decision making. There are also no specific sustainability linked disclosure requirements nor is there a specific obligation to consider ESG factors. From a Swiss regulatory perspective, financial institutions should (at least indirectly) take into account climate risks, especially when it comes to risk management considerations. Although, climate risks do in general not constitute a risk category itself, they can crystallize under certain other risk categories. Also, financial institutions need to consider climate risks within their duties of care and loyalty in connection with the risk assessment and education of their clients.

In addition to financial markets laws and regulations, self-regulation plays an important role in the Swiss financial framework. Absent any explicit legal basis for sustainability and climate risk related considerations, self-regulatory organizations (such as the Swiss Sustainable Finance Organization (“SSF“)) are important to – in a first step – set standards and provide guidance. SSF’s studies aim at promoting sustainable investments and to strengthen Switzerland’s position in the global financial markets for sustainable finance. Sustainable Finance is also a strategic priority matter of the Swiss Bankers Association (“SBA“). Pursuant to the SBA, Switzerland has the potential to become a leading financial center for sustainable finance if, among others, institutional investors are encouraged to take ESG factors into account in their investment strategy and by way of promoting investments in sustainable financial products (e.g. through tax incentives and elimination of tax burdens).

b) European Union

In March 2020, the final EU Taxonomy Technical Report was published setting standards for a uniform classification and designation framework for sustainable financial products and for sustainability linked disclosures which could tackle lack of benchmark consensus and offers market participants with coherent definitions. Further, the EU Action Plan (March 2018) has, among others, explicitly required (i) to clarify institutional investors’ and asset managers’ duties on sustainability and to increase transparency on their strategy and climate-related exposures and (ii) to strengthen sustainability disclosure. This has been achieved and implemented with the Disclosure Regulation (EU/2019/2088) which entered into effect in November 2019. This regulation implements harmonised rules for financial market participants and financial advisers on transparency with regard to the integration of sustainability risks and the consideration of adverse sustainability impacts in their processes and the provision of sustainability related information with respect to financial products.

Also, in connection with the revision of the Capital Adequacy Directive and Regulation (CRD V and CRR II), it is being discussed whether green / brown factors should be considered in connection with the risk weighting of regulatory capital. In addition, it is contemplated that systemically important financial institutions are explicitly required to disclose ESG-related risks. Further, the European Banking Authority has been mandated to investigate whether ESG factors should form part of the regulatory supervision.

4) Concluding thoughts

Climate change triggers, among other things, very significant costs and there does not seem to be any doubt that sustainable investments in the trillions are required to address climate change effectively. Various ESG financing methods provide investment opportunities to a broad range of potential participants and investors and thereby increase investments made / funds raised through sustainable finance. While investments in sustainable financial products or green bond issuances / sustainable borrowings were in the past mainly driven by philanthropic or reputational reasons, recent developments show a trend that these instruments and transactions become more and more important and there is also a clear trend towards ESG disclosure and sustainability considerations becoming part of the legal and regulatory framework.

Charlotte Rüegg (charlottesophie.rueegg@lenzstaehelin.com)