On 17 December 2021, Parliament concluded a legislative project that had taken more than ten years to complete. The main goal was to enable the issuance of domestic bonds free of withholding tax and thus strengthen the Swiss capital market. Further, transfer stamp duty on domestic bonds will also be abolished. The following article will discuss what the consequences of this reform are.

By Stefan Oesterhelt / Philippe Gobet (Reference: CapLaw-2022-05)

1) Introduction

The goal to strengthen the Swiss capital market is achieved by the abolition of withholding tax on bond interest already proposed by the Federal Council in its dispatch of 14 April 2021 (see Oesterhelt/Gobet, CapLaw-2021-35; Oesterhelt/Opel, Reform der Verrechnungssteuer, EF 8/21, p. 435) (see Section II below). The introduction of a paying agent tax, which was the core of the earlier reform proposals (see Oesterhelt, CapLaw-2020-41), has been dispensed with.

However, Parliament has made considerable changes to the Federal Council’s bill. In particular, a transitional provision was introduced according to which only new issues are affected by the abolition of withholding tax (see Section II.B below).

On the other hand, in line with the Federal Council’s proposal, Parliament adopted the abolition of the transfer stamp duty on domestic bonds (see Section V below).

2) Abolition of withholding tax on bond interest

a) Principle

Interest and equivalent income on domestic bonds is subject to withholding tax of 35% pursuant to article 4(1)(a) Federal Withholding Tax Act (WTA). This means that domestic groups almost always issue bonds that are to be placed internationally via a foreign group company in order to avoid the withholding tax. As of 1 January 2023, this will probably no longer be necessary.

The term “obligation” within the meaning of article 4(1)(a) WTA is extremely broad and can also cover syndicated loan agreements. As a result, loan agreements with a domestic debtor (or possibly also a domestic guarantor) are currently regularly subject to the so-called 10/20 non-bank rules in order to prevent a syndicated loan from being reclassified as a “bond” (Anleihensobligation) or debenture (Kassenobligation) subject to withholding tax. These restrictions should be unnecessary as of 1 January 2023.

Structured products with an interest component (e.g. reverse convertibles) are also regularly considered bonds within the meaning of article 4(1)(a) WTA, which is why these are today usually issued from abroad even if issued for the Swiss market. This will also no longer be necessary. In the future, structured products will be subject to withholding tax only if they are fund-like structured products governed by article 4(1)(c) WTA (i.e. in cases of tax evasion) or if income qualifies as benefit in kind within the meaning of article 4(1)(b) WTA.

The abolition of withholding tax on bond interest is clearly to be welcomed despite the associated weakening of the safeguarding purpose (Sicherungszweck) of withholding tax. The paying agent tax originally favoured by the Federal Council would have strengthened the safeguarding purpose of the withholding tax for income tax, but at the same time would have been extremely complicated to implement in practice.

b) Restriction to new issues (article 70e nWTA)

According to article 70e D-WTA in the Federal Council’s version of 14 April 2021, withholding tax would have been abolished for all interest due from 1 January 2023. In other words, interest on bonds already issued would also have been exempt from withholding tax.

However, article 70e nWTA now adopted by Parliament provides that withholding tax will continue to be levied on interest on bonds “formally issued by a resident” before 1 January 2023. This essentially avoids the tax losses associated with the abolition of withholding tax on bond interest for many years without harming the objective of the proposal or having a negative impact on the domestic capital market. Since the cost-benefit ratio of the reform is significantly improved by the restriction to new issues, such a transitional provision has previously already been called for by the authors (see Oesterhelt/Gobet, CapLaw-2021-35).

c) Repatriation of foreign issues and refinancing of domestic issues

The limitation of article 70e nWTA to “bonds formally issued by a resident” clarifies that the replacement of a foreign issue by a domestic issue (repatriation) is not affected by the provision of article 70e nWTA. Consequently, a transfer of the seat of a foreign finance company to Switzerland does not result in the bonds issued by this company before 1 January 2023 becoming subject to withholding tax. The same applies to a repatriation of a foreign issue through a change of issuer (issuer substitution).

Article 70e nWTA is to be understood strictly formally. The refinancing of a domestic issue subject to withholding tax by a domestic issue made on or after 1 January 2023 cannot be regarded as a “new issue” subject to withholding tax.

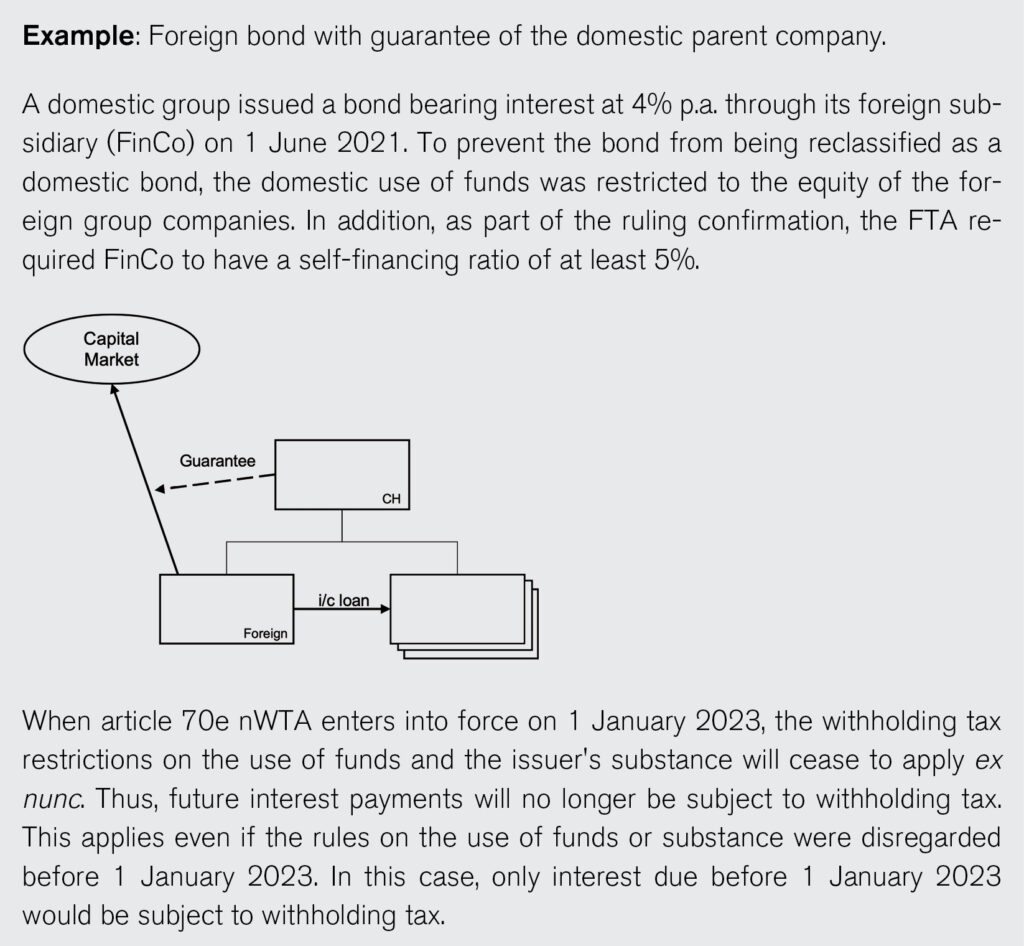

d) Foreign issues with restrictions on the use of funds

According to the current practice of the Federal Tax Administration (FTA), foreign issues guaranteed by a domestic company may, under certain circumstances, be considered a domestic issue subject to withholding tax if the domestic use of funds (inländische Mittelverwendung) exceeds the equity of the foreign companies of the group (see Oesterhelt, CapLaw-2018-01). These restrictions on the use of funds will cease to apply as of 1 January 2023. This also applies to existing issues, as such issues are not “bonds formally issued by a resident”. Thus, for foreign issues guaranteed by a domestic company, the restrictions on the use of funds no longer have to be complied with as of 1 January 2023 if the terms and conditions of the bond permit this (see Example).

Consequently, the same applies to foreign issues for which the restriction on the use of funds was already violated before 1 January 2023 and which were thus reclassified as domestic issues subject to withholding tax. These are not “bonds formally issued by a resident” and are therefore not affected by the transitional provision of article 70e nWTA. The previously applicable principle of “once a domestic issue, always a domestic issue” (see Oesterhelt, CapLaw-2018-01) is thus overridden by the legislative amendment of 17 December 2021 (see Example).

The same applies to an issue by a foreign finance company that was qualified as a resident by the FTA due to the lack of substance of the issuer abroad pursuant to article 9(1) WTA. The requirements imposed by the FTA regarding the substance abroad no longer need to be complied with as of 1 January 2023, without this resulting in withholding tax consequences on interest of bonds issued before 1 January 2023. If the required substance abroad did not exist before 1 January 2023, withholding tax is due on the interest due dates before 1 January 2023, but not on later interest due dates.

In the case of a bullet repayment syndicated loan (endfällige Anleihensobligation) or debenture (endfällige Kassenobligation), a breach of the restriction on the use of funds or the substance requirements for the foreign issuer before 1 January 2023 is harmless if the interest is due only after article 70e nWTA comes into force.

e) Relationship to withholding tax pursuant to article 94 DTA or article 35(1)(e) THA

The tax at source (Quellensteuer) pursuant to article 94 Federal Direct Tax Act (DTA) or article 35(1)(e) Federal Tax Harmonisation Act (THA) on bonds secured by domestic real estate is currently pushed back to the extent that the interest payment is subject to withholding tax. The abolition of withholding tax on bonds leads to a revival of the withholding tax according to article 94 DTA or article 35(1)(e) THA.

However, the transitional provision of article 70e nWTA prevents the tax at source from being due again on bonds already issued before 1 January 2023 and thus subject to withholding tax.

For domestic bonds issued after 1 January 2023 that are secured by domestic real estate, however, the tax at source must be considered in accordance with the provision in article 94 DTA or cantonal law modelled on article 35(1)(e) THA. Since such bonds are no longer subject to withholding tax, the tax at source on interest payments to foreign creditors and usufructuaries must in principle be levied again in the future. The only exception is if a double taxation agreement pushes back Switzerland’s right of taxation, i.e. assigns the exclusive right of taxation to the state of residence. In such a case, there is an exemption at source. In the case of loans secured by domestic real estate, transfers are therefore usually contractually limited to so-called “treaty lenders”, i.e. lenders that are resident in a state with which Switzerland has concluded a double taxation agreement that reserves the right of taxation exclusively to the state of residence (“zero rate on interest”).

3) Customer credit balances (article 4(1)(a) nWTA)

The amendments proposed by the Federal Council on withholding tax on client deposits pursuant to article 4(1)(d) WTA (now article 4(1)(a) nWTA) were adopted unchanged. If the bill is accepted, the 100 non-bank rule will be a thing of the past (as will the 10/20 non-bank rules).

4) Manufactured payments (article 4(1)(d) nWTA)

The legal provision proposed by the Federal Council for levying withholding tax on manufactured payments (article 4(1)(d) nWTA) was also adopted unchanged by Parliament despite the criticism that had been voiced in this regard. In particular, Parliament ultimately refrained from limiting article 4(1)(d) nWTA to manufactured payments by domestic debtors, as originally demanded by the National Council.

The declared aim of article 4(1)(d) nWTA is to be able to continue practice lived previously through the “Gentlemen’s Agreement” (see Oesterhelt/Gobet, CapLaw-2021-35, Section III.E), which was unhinged by the ruling of the Federal Supreme Court of 21 November 2017 (2C_123/2016). In this respect, it will be decisive how the (in our opinion somewhat unfortunate) wording of article 4(1)(d) nWTA is implemented in the practice of the FTA.

5) Abolition of transfer stamp duty on domestic bonds

As already proposed by the Federal Council, domestic bonds will no longer be considered taxable securities for the purposes of transfer stamp duty. Since primary market transactions with domestic bonds (article 14(1)(a) Federal Stamp Duties Act [SDA]) as well as the redemption (Rückgabe zur Tilgung) (article 14(1)(e) SDA) are already exempt from transfer stamp duty, the amendment primarily affects secondary market transactions with domestic bonds (with a tenor of above one year, article 14(1)(g) SDA).

Since domestic bonds will no longer be taxable securities within the meaning of article 13(2) SDA, they are also no longer relevant for the definition of securities dealer under article 13(3)(d) SDA.

For the same reason, domestic issues of structured products with a bond component will no longer be subject to transfer stamp duty.

Domestic bonds issued prior to the legislative amendment will also no longer be taxable securities within the meaning of article 13(2) SDA. This also applies if a formerly foreign issuer relocates its seat to Switzerland. However, due to the formal nature of stamp duties, it is not sufficient if only the effective place of administration of the issuer is transferred to Switzerland.

For the transition, the relevant point in time is the entry into of the (unconditional) contractual obligation in relation to the transaction (Verpflichtungsgeschäft) rather than the transfer of ownership under civil law (Verfügungsgeschäft). This is because the entry into of the transaction is the point in time at which the stamp duty claim arises pursuant to article 15(1) SDA.

6) Turnover tax on foreign bonds (article 13(2)(abis) nSDA)

Bonds issued by a foreigner, on the other hand, are still taxable securities for the purposes of transfer stamp duty. Due to the repeal of article 13(2)(a)(1) SDA, a new legal basis had to be created in article 13(2)(abis) nSDA in this regard.

Trading in foreign bonds (secondary market transaction) as well as the issuance of foreign bonds denominated in Swiss francs (primary market transaction) will continue to be subject to the transfer stamp duty if a domestic securities dealer is involved in the transaction as a party or intermediary. However, as before, the redemption (Rückgabe zur Tilgung) (article 14(1)(e) SDA) and secondary market transactions in which either the buyer or the seller is a foreign contracting party (article 14(1)(h) SDA) are exempt.

Bonds issued by a foreign branch of a domestic company are – as is already the case today – treated as “bonds issued by a foreigner” within the meaning of article 13(2)(abis) nSDA at least if the branch is a regulated bank branch.

7) Entry into force

Parliament has set the abolition of withholding tax on bond interest and the entry into force of the transitional provision of article 70e nWTA for 1 January 2023. This applies even if the referendum that has already been initiated is successful but the people approve the bill. The referendum period expires on 7 April 2022, so that a referendum vote could take place in September or November 2022.

The entry into force of the other amendments to the WTA and the SDA will be determined by the Federal Council. In this regard, it is highly uncertain whether these can also enter into force as early as 1 January 2023. The changes in the area of customer deposits as well as the transfer stamp duty make it necessary for the banks to adapt their IT systems, for which a certain lead time is needed. This applies even if the referendum deadline were to expire unused.

Stefan Oesterhelt (stefan.oesterhelt@homburger.ch)

Philippe Gobet (philippe.gobet@homburger.ch)