The regulatory framework for the supervision of Swiss insurance undertakings is currently undergoing a partial revision, which, inter alia, will bring changes regarding risk-absorbing capital instruments. This article provides an overview over the capital requirements of Swiss insurers and sets out the treatment of risk-absorbing capital instruments under both the current and future regulations.

By Hansjürg Appenzeller / Vanessa Isler (Reference: CapLaw-2022-34)

1) Revision of Insurance Regulations

The regulatory framework for the supervision of Swiss insurance undertakings is currently undergoing a partial revision. Several years in the making, on 18 March 2022, the Swiss Parliament finally adopted the partial revision of the Act on the Supervision of Private Insurance Undertakings (Versicherungsaufsichtsgesetz; Insurance Supervisory Act (ISA), and as revised by the partial revision (nISA)), which is currently expected to enter into force in mid-2023. On 17 May 2022, the Swiss Federal Department of Finance published the draft amendment of the Ordinance on the Supervision of Private Insurance Undertakings (Aufsichtsverordnung, Insurance Supervisory Ordinance (ISO) and as revised by the draft amendment (E-ISO)), aimed at implementing the revised provisions contemplated in the nISA. The consultation period for the E-ISO expired on 7 September 2022. Based on this consultation, further amendments to the E-ISO may be expected. The following considerations are based on the E-ISO as published on 17 May 2022 and assume that there will be no major changes with respect to regulatory capital in the final amended ISO.

While the main focus of the revision of the ISA is the introduction of a restructuring regime for insurance undertakings, the modernization of the rules governing insurance intermediation and the creation of a supervisory and regulatory system based on varied client protection needs, the E-ISO is also set to bring important changes relating to risk-absorbing capital instruments.

2) Treatment of Risk-Absorbing Capital Instruments under the Old and New Regime

a) Overview over capital requirements of insurers

Generally, insurance undertakings are required to have sufficient free and unencumbered capital to cover their entire business activities (article 9(1) ISA / articles 9 et seq. nISA). This is measured by way of the Swiss Solvency Test (SST), which, simply put, plots the capital an insurance undertaking should have, quantifying, among others, the market, credit and underwriting risks to which it is exposed (Zielkapital; target capital), against the available regulatory capital (risikotragendes Kapital; risk-bearing capital).

The results of the SST are expressed by way of the SST ratio, which, in simplified terms, is the ratio (expressed as a percentage) of the risk-bearing capital divided by the target capital in any given year. The SST ratio should always be above 100%. In practice, the average SST ratio for insurance undertakings is much higher, amounting to, on average, 264% for non-life insurers, 236% for life insurers and 203% for reinsurers in 2021 (cf. Report on the Swiss Insurance Market 2021, published by the Swiss Financial Market Supervisory Authority FINMA (FINMA) on 9 September 2022).

b) Risk-absorbing capital instruments as part of risk-bearing capital

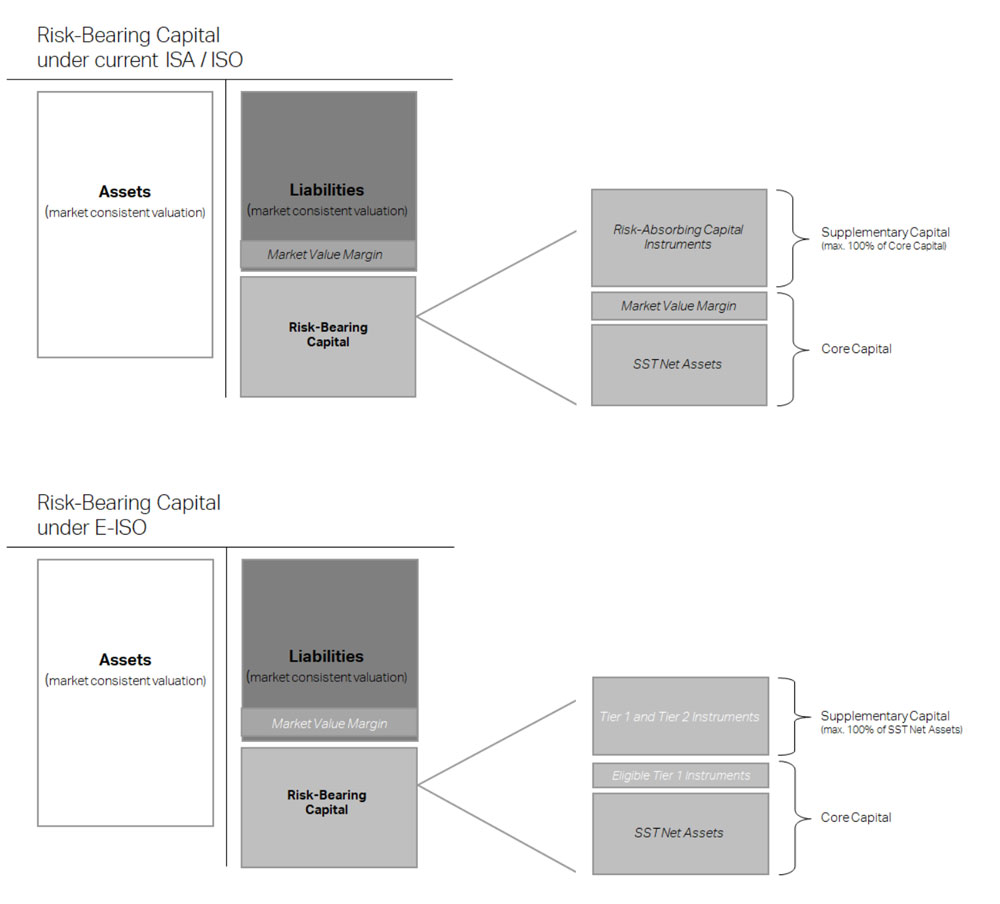

The risk-bearing capital is made up of the core capital (Kernkapital) and the supplementary capital (ergänzendes Kapital).

i. Core capital (Kernkapital)

The core capital is calculated, both under the old and new regime, on the basis of the SST net assets which are determined based on a total balance sheet approach (i.e., the SST balance sheet contains all economically relevant balance sheet items of the insurance undertaking including off-balance sheet items but excluding any corporate tax items), minus certain deductions (article 48(1) ISO / article 9a para. 1 nISA and article 32(4) E-ISO). While different terms are used for describing the valuation methodology applied to determine the value of the assets and liabilities shown in the SST balance sheet under the old and new regime (market consistent (marktnah) valuation and market consistent (marktkonform) valuation, respectively), no major deviations in the valuation of the insurance undertaking’s assets and liabilities are expected in practice.

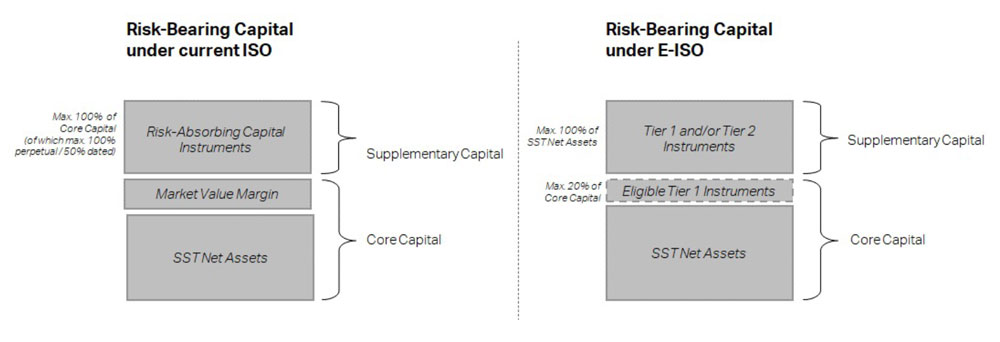

Under the old regime, the market value margin (Mindestbetrag), which is also included in the determination of the market consistent (marktnah) value of liabilities (article 41(3) and Annex 3 ISO), is added to the SST net assets and, thus, considered positively in calculating the core capital (article 48(1) ISO). The market value margin is calculated as the sum of the expected values of the discounted capital costs of each one-year risk capital over the future one-year periods required by the insurance undertaking to fulfil its insurance liabilities. As such, the market value margin is intended to cover the cost of holding of the regulatory required capital for the run-off of the in-force business in the event an insurance undertaking ceases business operations. However, it should be noted that, pursuant to the E-ISO, the market value margin will no longer be added to the SST net assets when calculating the core capital (but still considered in the determination of the market consistent (marktkonform) value of liabilities, article 30(4) E-ISO). Instead, under the E-ISO, the core capital equals the sum of the SST net assets plus the Tier 1 risk-absorbing capital instruments, to the extent eligible for inclusion in the core capital (cf. article 32(2) E-ISO).

ii. Supplementary capital (ergänzendes Kapital)

Swiss capital regulation allows an insurance undertaking to augment its regulatory capital by adding so-called supplementary capital (ergänzendes Kapital) to the core capital. The supplementary capital consists of risk-absorbing capital instruments (risikoabsorbierende Kapitalinstrumente), in particular subordinated bonds and loans, which have certain prescribed equity-like features (hybrid capital). Risk-absorbing capital instruments can be included in the risk-bearing capital or considered in the target capital.

3) Current Requirements for the Eligibility of Risk-Absorbing Capital Instruments

The currently applicable regulation separates supplementary capital into upper and lower supplementary capital. Upper supplementary capital (oberes ergänzendes Kapital) is perpetual (i.e., it does not have a fixed maturity date) and can be included in the risk-bearing capital up to a maximum of 100% of the core capital. Lower supplementary capital (unteres ergänzendes Kapital), on the other hand, has an original maturity of at least five years. It can be included in the risk-bearing capital up to a maximum of only 50% of the core capital. In addition, in the last five years of the relevant instrument’s term, the amount eligible for inclusion in the risk-bearing capital is reduced annually by an amount equal to 20% of the original nominal amount of the instrument (articles 47 and 49 ISO).

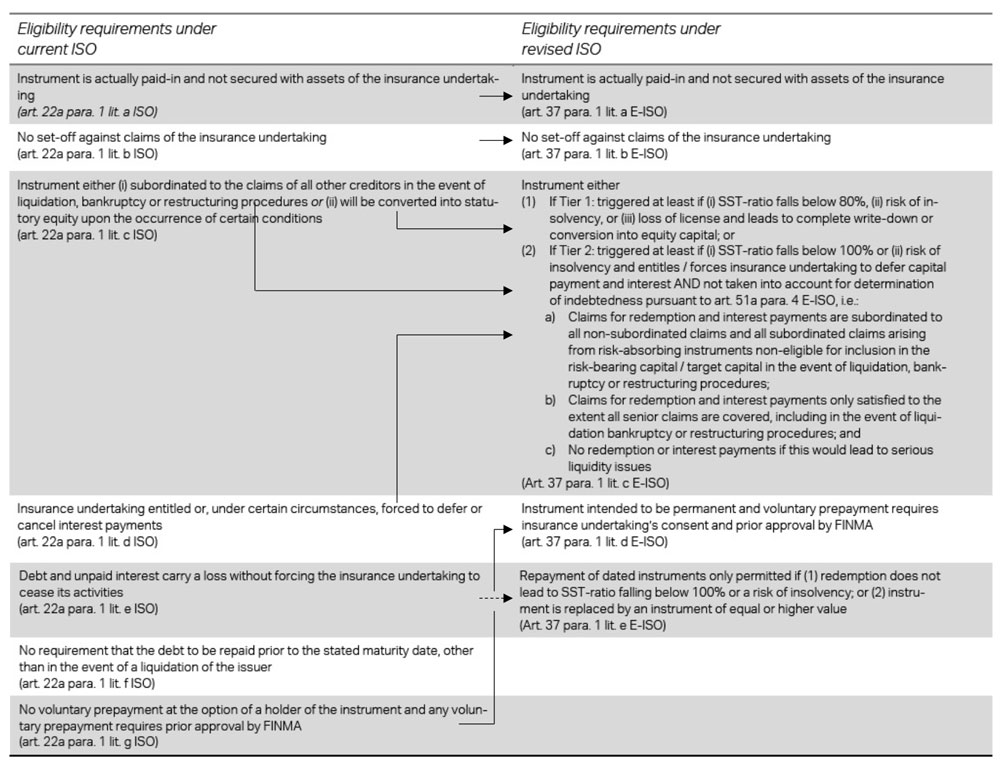

In order to qualify as risk-absorbing instruments pursuant to article 22a ISO and therefore be eligible for inclusion in the insurance undertaking’s risk-bearing capital or consideration in its target capital, the instruments have to fulfill the following requirements:

– the instrument is actually paid-in and not secured with assets of the insurance undertaking;

– the terms of the instrument do not allow any set-off against claims of the insurance undertaking;

– the terms of the instrument irrevocably stipulate that it is either (i) subordinated to the claims of all other creditors in the event of liquidation, bankruptcy or restructuring procedures with respect to the insurance undertaking, or (ii) will be converted into statutory equity upon the occurrence of certain conditions;

– the terms of the instrument entitles or under certain circumstances forces the insurance undertaking to defer or cancel interest payments;

– the terms of the instruments stipulate that debt and unpaid interest carry a loss without forcing the insurance undertaking to cease its activities;

– the terms of the instrument does not in any way require the debt to be repaid prior to the stated maturity date, other than in the event of a liquidation of the issuer; and

– the instrument may not be repaid voluntarily at the option of a holder of the instrument and any voluntary prepayment requires prior approval by FINMA (which shall be granted if the insurance undertaking can show that such prepayment will not jeopardize its solvency).

Not only the issuer of the risk-absorbing capital instrument can benefit from their inclusion in the risk-bearing capital or consideration in the target capital. Inclusion or consideration is also permitted on the group level with respect to the relevant consolidated group SST (article 198 ISO).

4) Changes Proposed for the Eligibility of Risk-Absorbing Capital Instruments

Insurance undertakings will continue to be able to include risk-absorbing capital instruments in the risk-bearing capital or consider such instruments in the target capital under the E-ISO. However, the E-ISO proposes a number of key changes, which are intended mainly to integrate into the new restructuring regime for insurance undertakings and to increase comparability with the capital requirements under EU insurance regulation (i.e., “Solvency II”).

a) Separation of risk-absorbing capital instruments into Tier 1 and Tier 2 instruments

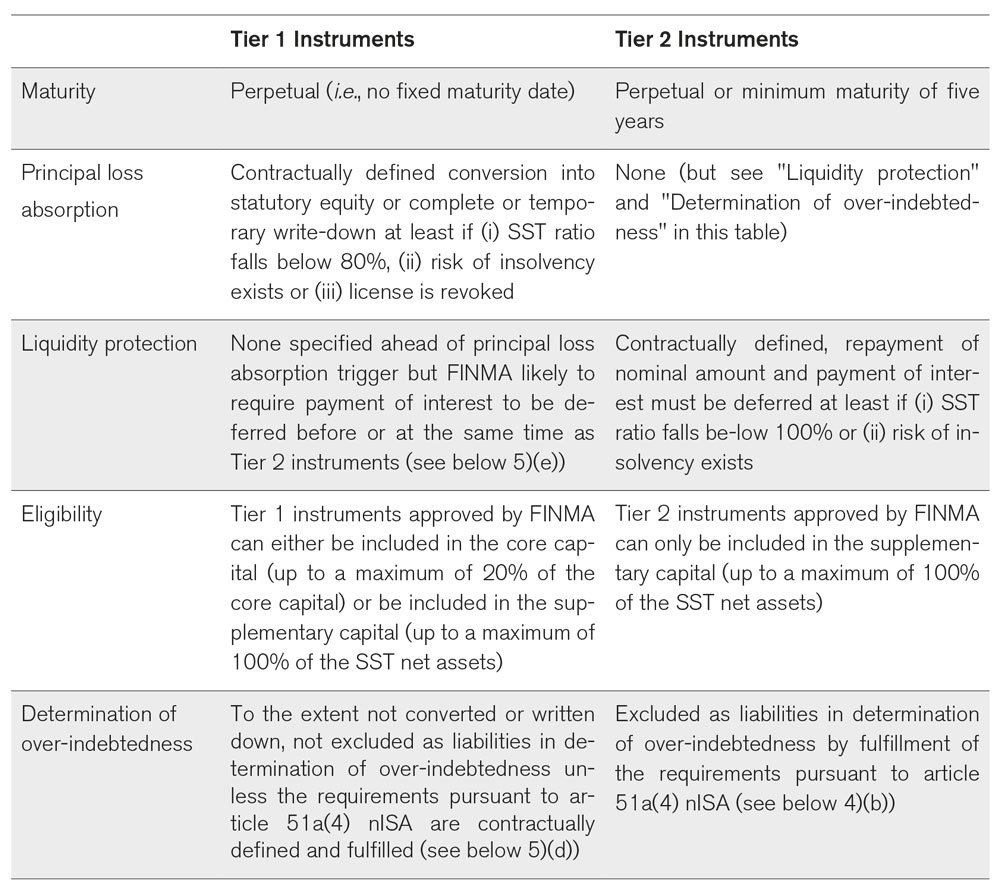

By analogy with Additional Tier 1 Capital (AT1) and Supplementary Capital (Tier 2 Capital, T2) under the tiered capital requirements for banks set out in the Ordinance on the Capital Adquacy and Risk Diversification of Banks and Securities Firms (Eigenmittelverordnung; CAO), the E-ISO proposes to divide risk-absorbing capital instruments into Tier 1 instruments and Tier 2 instruments. Tier 1 instruments must be perpetual whereas Tier 2 instruments may be perpetual or dated. However, the requirements for Tier 1 and Tier 2 instruments differ in more meaningful ways based on their capacity to absorb losses while the (re-)insurer remains a going concern (cf. articles 34, 37 and 38 E-ISO):

In analogy to Additional Tier 1 Equity (AT1) and Supplementary Capital (Tier 2 Capital, T2) under the tiered capital requirements for banks set out in the Ordinance on the Capital Adquacy and Risk Diversification of Banks and Securities Firms (Eigenmittelverordnung; CAO), the E-ISO introduces two tiers of risk-absorbing capital instruments which are triggered by separate events and lead to different consequences. Tier 2 instruments are triggered earlier on and only cause for any redemptions and payments of interest to be deferred. Tier 1 instruments are triggered if the risk-bearing capital clearly no longer covers the target capital and necessarily lead to a write-down or a conversion into equity, whichever is specified in the terms of the relevant instrument.

Despite the explanatory report to the E-ISO extolling the virtues of Tier 1 insturments, we do not expect to see a large number of Swiss insurance undertakings issuing Tier 1 instruments in the near future, both due to the increased cost of capital for the issuance of Tier 1 instruments and the limited demand given that Tier 2 instruments can also be included in the risk-bearing capital up to 100% of the SST net assets.

In addition to the introduction of tiered risk-absorbing capital instruments, the E-ISO no longer includes the market value margin for the calculation of the core capital (see above 2)(b)(i)). Side-by-side the risk-bearing capital under the current ISO and the E-ISO looks as follows:

b) Future requirements for the eligibility of risk-absorbing capital instruments

Under the E-ISO, risk-absorbing capital instruments will continue to have to meet certain requirements in order to be eligible for inclusion in the core capital or supplementory capital, as the case may be.

While the eligibility requirements for risk-absorbing capital under article 37 E-ISO to a certain extent mirror the current requirements under article 22a ISO, there are some key differences to observe under the E-ISO. The main difference is obviously the introduction of two different tiers of risk-absorbing capital instruments (see above under 4)(a)). However, article 37 E-ISO also introduces additional changes. Firstly, Tier 2 instruments (as to Tier 1 instruments, see below 5)(e)) have to additionally fulfill the requirements set out in article 51a(4) nISA for an eligible risk-absorbing capital instrument to be excluded for the purposes of determining the issuer’s over-indebtedness. This important provision prevents the situation where somewhat ironically the claims arising from a risk-absorbing capital instrument might themselves trigger an over-indebtedness and thereby render the instrument’s loss-absorbing function moot. Secondly, article 37(1) lit. e E-ISO introduces the new requirement that any repayment of Tier 2 instruments with a fixed maturity is only permitted (i) to the extent that such repayment does not cause the SST ratio to fall below 100% nor cause a risk of insolvency or (ii) if such Tier 2 instrument is replaced by another (Tier 1 or Tier 2) instrument which is not only of equal or higher quality but also has an equal or preferable impact on the SST calculation with respect to the amount included in the risk-bearing capital. However, article 37 E-ISO no longer a priori prevents prepayments prior to the stated maturity date of the relevant instrument (but still requires prior approval by FINMA). Article 37(1) lit. d E-ISO, on the other hand, should be understood as an editorial improvement to clarify article 22a(1) lit. g ISO and does not intend to introduce any substantive change.

Pursuant to FINMA’s current practice, risk-absorbing instruments may contain a moderate incentive (e.g., interest step up) for repayment without limitations as to the time when such incentive applies. Article 37(3) E-ISO codifies this practice for Tier 2 instruments, but such incentive may only kick in ten years after the issue date of the instrument.

c) Eligibility of risk-absorbing capital instruments on group level

Under the current rules, article 198 ISO allows insurance groups to include risk-absorbing capital instruments in the group risk-bearing capital with respect to the consolidated group SST. Article 198d E-ISO, which differentiates between two scenarios, will introduce more stringent requirements for the eligibility of risk-absorbing capital instruments for inclusion in the risk-bearing capital or consideration in the target capital with respect to the consolidated group SST.

The first scenario captures the issuance of risk-absorbing capital instruments by a Swiss insurance undertaking which is part of an insurance group and is itself subject to the SST. In order to be eligible for inclusion or consideration on a group level, the relevant instruments must meet the following requirements (article 198d(1) E-ISO):

– the risk-absorbing capital instruments fulfill the requirements of article 37 E-ISO with respect to the issuing group company;

– the respective Tier 1 or Tier 2 trigger also makes reference to the SST ratio of the consolidated group SST and the insolvency risk of the top group company; and

– if such risk-absorbing capital instruments are guaranteed by another group company, (i) the definition of “insolvency risk” pursuant to article 37(1) lit. c E-ISO also extends to such group company and (ii) it is ensured that the guarantees regarding the risk-absorbing capital instruments will not be considered in the determination of the guaranteeing group company’s over-indebtedness.

The second scenario addresses the issuance of risk-absorbing capital instruments by a member of an insurance group that is itself not subject to the SST. In order to be eligible for inclusion or consideration on a group level, the relevant instruments must meet the following requirements (article 198d(2) E-ISO):

– the risk-absorbing capital instruments fulfill the requirements of article 37 E-ISO with respect to the issuing group company;

– the respective Tier 1 or Tier 2 trigger also makes reference to the SST ratio of the consolidated group SST and the insolvency risk of the top group company; and

– if such risk-absorbing capital instruments are not guaranteed by another group company, it is ensured that the risk-absorbing capital instruments will not be considered in the determination of the issuing group company’s over-indebtedness; or

– if such risk-absorbing capital instruments are guaranteed by another group company, (i) the definition of “insolvency risk” pursuant to article 37(1) lit. c E-ISO also extends to such guaranteeing group company and (ii) it is ensured that the guarantees regarding the risk-absorbing capital instruments will not be considered in the determination of the guaranteeing group company’s over-indebtedness.

By extending the decisive triggers and references regarding insolvency risk to the issuing group company, the guaranteeing group company and/or the top group company, the revised ISO aims to prevent financial resources flowing out of the group due to payments arising under risk-absorbing capital instruments in situations where the group and the top group company no longer meet the requirements of the consolidated SST and face the risk of insolvency, respectively.

d) Transitional provisions

Article 216c E-ISO allows for grandfathering periods for risk-absorbing capital instruments issued under the current ISO and approved as eligible by FINMA:

– Instruments that do not meet the eligibility requirements of article 37 E-ISO can be included in the supplementory capital or considered in the target capital until the earlier of (i) the repayment date and (ii) 10 years following the revised ISO entering into force (i.e., expected to run until mid-2033).

– Instruments are exempt from a bail-in by way of conversion into equity or write-down pursuant to article 52d(4) nISA for a maximum of 10 years following the revised ISO entering into force.

5) Issues in Practice

Despite not even having entered into force, the revised rules on the eligibility of risk-absorbing capital instruments have already brought to light a number of issues which merit a closer look, if not clarifying statements in the final version of the revised ISO.

a) Infection risk if eligibility of risk-absorbing capital instrument is revoked during their term

Article 51(4) lit. a nISA discounts risk-absorbing capital instruments from being included in the determination of the issuing entity’s over-indebtedness if they fulfil certain requirements (see above 4)(b)). If FINMA revokes the relevant instruments eligibility, in particular due to the lapse of the grandfathering period for legacy instruments (see above (4)(d)), claims arising out of such instruments (if they do not fulfil the requirements of article 51(4) nISA) would suddenly be included in the determination of the issuer’s over-indebtedness and could therefore trigger an insolvency event. In practice, however, if such instruments do are no longer eligible for inclusion in the risk-bearing capital any more (e.g., at the end of the grandfathering period), they will likely be called for redemption. The reason being that such instruments would then constitute an overly expensive form of funding.

b) Effect of risk-absorbing capital instruments on the SST

Pursuant to article 34(1) lit. a E-ISO, the effect of risk-absorbing capital instruments on the SST by inclusion in the risk-bearing capital or consideration in the target capital in terms of amounts is determined by (a) the market consistent value (i.e., the financial expenditures of the issuer to fulfil the relevant liabilities; cf. article 27 E-ISO) on the effective date of the instrument’s inclusion in the risk-bearing capital and (b) the effect on the target capital for consideration in the target capital.

In our view it is not sufficiently clear how the market consistent value of the risk-absorbing capital instrument would be recognized in the SST net assets and eligible with respect to the risk-bearing capital. For instance, if such instrument traded at 80% of its nominal value on the effective date of its inclusion in the risk-bearing capital, article 34(1) lit. a E-ISO implies that it would only be included to that extent in the risk-bearing capital, but for purposes of the SST net asset calculation added to the liabilities at 100% of its nominal value.

c) Treatment of guarantee claims regarding claims under risk-absorbing capital instruments in the over-indebtedness of a guaranteeing group company

If a group company guarantees a risk-absorbing instrument, article 198d(1) lit. c and (2) lit. d E-ISO require that it is ensured that the guarantees regarding the risk-absorbing capital instruments will not be considered in the determination of the guaranteeing group company’s over-indebtedness. However, article 51a(4) nISA, which exempts claims stemming from risk-absorbing capital instruments from being included in the determination of over-indebtedness does not specifically refer to the guarantee claims which cover the relevant claims arising out of the risk-absorbing capital instruments.

In our view, this can only be an editorial error which crept into the nISA when the relevant paragraph was introduced during the parliamentary discussions. Firstly, the explanatory report to the E-ISO specifically points out with reference to article 198d(2) lit. c E-ISO that ensuring that risk-absorbing capital instruments are not included in the determination of the issuing group company’s of overindebtedness is equivalent to a contractual assurance that at least no financial recources can flow out of the group by servicing claims of the creditors of the risk-absorbing capital instruments. While article 198d(2) lit. c E-ISO refers only to the scenario where there is no group-internal guarantee, article 198d(2) lit. d E-ISO, referring to risk-absorbing capital instruments that are guaranteed by another group company, mirrors the same requirements with respect to the guaranteeing group company.

Structurally, this allows the conclusion that it is sufficient if the terms of the relevant instruments ensure that that no financial resources can flow out of the group by servicing the creditor claims against the guarantor of the risk-absorbing capital instruments. This, in turn, can be accomplished by having the terms of the underlying guarantee comply with the requirements set out in article 51a(4) nISA per analogy.

Finally, if article 51a(4) nISA did not apply to claims arising from a guarantee on claims for repayment and payment of interest arising from risk-absorbing capital instruments, it would undermine the provisions entire purpose, namely to strengthen the insurance undertaking’s / insurance group’s capital situation in the event of insolvency. This is because taking the guarantee claim into account at the level of the guarantor could trigger the guarantor’s over-indebtedness, which in effect would likely result in a chain reaction within the insurance group, leading to the same results as if the capital claim and interest payments arising directly from the risk-absorbing capital instruments were included in the determination of the over-indebtedness of the issuer. Additionally, the only alternative to the above solution would be a subordination agreement with a moratorium (Stundung) (as required pursuant to Swiss corporate law for not considering debt in the determination of over-indebtedness), which in turn would trigger “cross-defaults” in other contracts (e.g., in standard market loan agreements and bond terms, under which any moratorium usually leads directly to an “event of default” and thus to an accelaration of the debt).

Essentially, this would make it impossible to issue risk-absorbing capital instruments with a guarantee from another group company, which in turn would make it significantly more expensive and more difficult for Swiss insurance groups to raise funds through the capital markets. Against this background, we would welcome a clarication in the final revised ISO.

d) Treatment of Tier 1 instruments in the determination of over-indebtedness

Other than Tier 2 instruments, article 37(1) lit. c E-ISO does not explicitly require Tier 1 in-struments to fulfil the requirements set out in article 51a(4) nISA. However, if these require-ments are not fulfilled, Tier 1 instruments can arguably not be excluded as liabilities for the purposes of determining the issuer’s over-indebtedness, which affects their loss absorbing properties. Therefore, an issuer is well advised to ensure that Tier 1 instruments also fulfil the requirements set out in article 51a(4) nISA and, thus, will not be considered as liabilities in the determination of the issuer’s over-indebtedness.

e) Absence of interest deferral in Tier 1 instruments

Tier 2 instruments are required to defer the repayment of nominal amount and the payment of interest at least if (i) the SST ratio falls below 100% or (ii) a risk of insolvency exists (article 37(1) lit. c E-ISO). By contrast, the E-ISO does not contain any deferral provisions for Tier 1 instruments. In practice, however, we would expect that the deferral with respect to Tier 2 instruments would be triggered before Tier 1 instruments are converted or written down.

In our assessment, that is an editorial oversight. It is not conceivable that Tier 2 instruments are required to defer interest while at the same time interest is paid on Tier 1 instruments prior to their conversion or write down. Therefore, we would expect FINMA to require the deferral of interest payments on Tier 1 instruments before or at the same time as such de-ferral is triggered with respect to Tier 2 instruments.

Hansjürg Appenzeller (hansjuerg.appenzeller@homburger.ch)

Vanessa Isler (vanessa.isler@homburger.ch)