The extensive understanding of the notion of activity as an “intermediary” in Swiss stamp duty law as interpreted by the Swiss Federal Tax Administration and confirmed by the latest case law of Swiss Supreme Court and Swiss Federal Administrative Court has significant practical consequences: Domestic M&A advisors, Family Offices as well as intragroup management companies could potentially qualify as “securities dealers” in terms of the Stamp Duty Act, as they act as “intermediary” on transactions involving taxable securities. Furthermore, Swiss securities transfer tax risks may arise if the domestic group parent company is involved as an “intermediary” in the sale or purchase of taxable securities.

By Stefan Oesterhelt / Miriam Kämpf (Reference: CapLaw-2023-05)

1) Introduction

The sale of shares of a domestic or foreign company is subject to 0.15% (domestic company) or 0.3% (foreign company) Swiss securities transfer tax (Umsatzabgabe) if a Swiss securities dealer is involved either as a party or an intermediary to a transaction.

The notion “intermediary” is therefore of great practical relevance since it results in a transaction being subject to Swiss securities transfer tax even if none of the parties is a Swiss securities dealer (e.g. because both parties are foreign resident companies). Since this notion is not defined in Swiss stamp duty law, its scope is not always clear. On 25 February 2021, the Swiss Supreme Court rendered an important decision in this respect about the involvement of a domestic group parent company in an M&A transaction (see below 3).

There is also a second meaning of the notion “intermediary” in Swiss stamp duty law. A Swiss domiciled entity or individual can become a “Swiss securities dealer” if its activity consists exclusively or to a substantial part in “intermediating the purchase and sale of taxable securities”. In the judgment of 23 November 2021, the Federal Administrative Court ruled on the circumstances under which an M&A advisory company qualifies as a securities dealer by virtue of its activity as “intermediary”.

2) Principles of Swiss securities transfer tax

a) Transactions subject to Swiss securities transfer tax

The Swiss securities transfer tax is payable on the transfer of taxable securities against consideration provided that a Swiss securities dealer is involved in the transaction, either as contractual party or as intermediary. The concept of “securities dealer” thus assumes a central importance.

b) Taxable securities

Taxable securities are in particular shares, bonds, units in collective investment schemes issued by a domestic or foreign person (e.g. shares in a Swiss or domestic company).

c) Transfer of ownership against consideration

The Swiss securities transfer tax is due if the transfer of ownership/legal title of the taxable securities is executed against payment. It is thereby irrelevant whether the transaction is executed in Switzerland or abroad.

d) Swiss securities dealer

The law on Swiss securities transfer tax contains a legal definition of the term Swiss securities dealer in Art. 13(3) Stamp Duty Act (SDA). This is intended to ensure special compliance with the requirement for clarity due to the central importance of the term “Swiss securities dealer”.

The Stamp Duty Act first declares Swiss banks and bank-like finance companies within the meaning of the Swiss Federal Banking Act (BA) as well as central counterparties within the meaning of the Swiss Federal Financial Market Infrastructure Act (FinMIA) to be securities dealers. Due to the reference to civil law legislation, these are sharply defined terms.

The Stamp Duty Act then designates Swiss corporations, cooperatives, and occupational pension institutions as securities dealers if, according to the last balance sheet, more than CHF 10 million of their assets consist of taxable securities within the meaning of Art. 13(2) SDA. Based on the formal understanding of this provision, this is also a very clear definition of the term.

Furthermore, according to the Stamp Duty Act, intermediaries of taxable securities also qualify as securities dealers. The Stamp Duty Act defines the intermediary as follows:

“Securities dealers are […] the domestic individual and legal persons and partnerships, domestic institutions and branches of foreign companies […], whose activity consists exclusively or to a substantial part in intermediating […] the purchase and sale of taxable securities as investment advisors or asset managers (intermediaries) (Art. 13(3)(b)(2) SDA)”

In contrast to the definitions of securities dealers listed above, the definition of intermediary contains numerous undefined legal terms and is accordingly far less clearly defined than the other securities dealer definitions.

A business established outside of Switzerland and not acting through a Swiss branch office is not a “Swiss” securities dealer. The same is true for a Swiss securities dealer’s branch office outside Switzerland.

e) Tax rate and trigger of the tax claim

The tax is levied on the consideration owed for the transfer of the securities. For securities issued by a Swiss issuer, the tax rate is 0.15%. For securities issued by a non-Swiss issuer, the tax rate is 0.3%. The tax is triggered when the contract for transfer of the taxable securities is concluded. If completion of the transaction is subject to non-fulfilled conditions, the tax is triggered only upon the transfer of the securities.

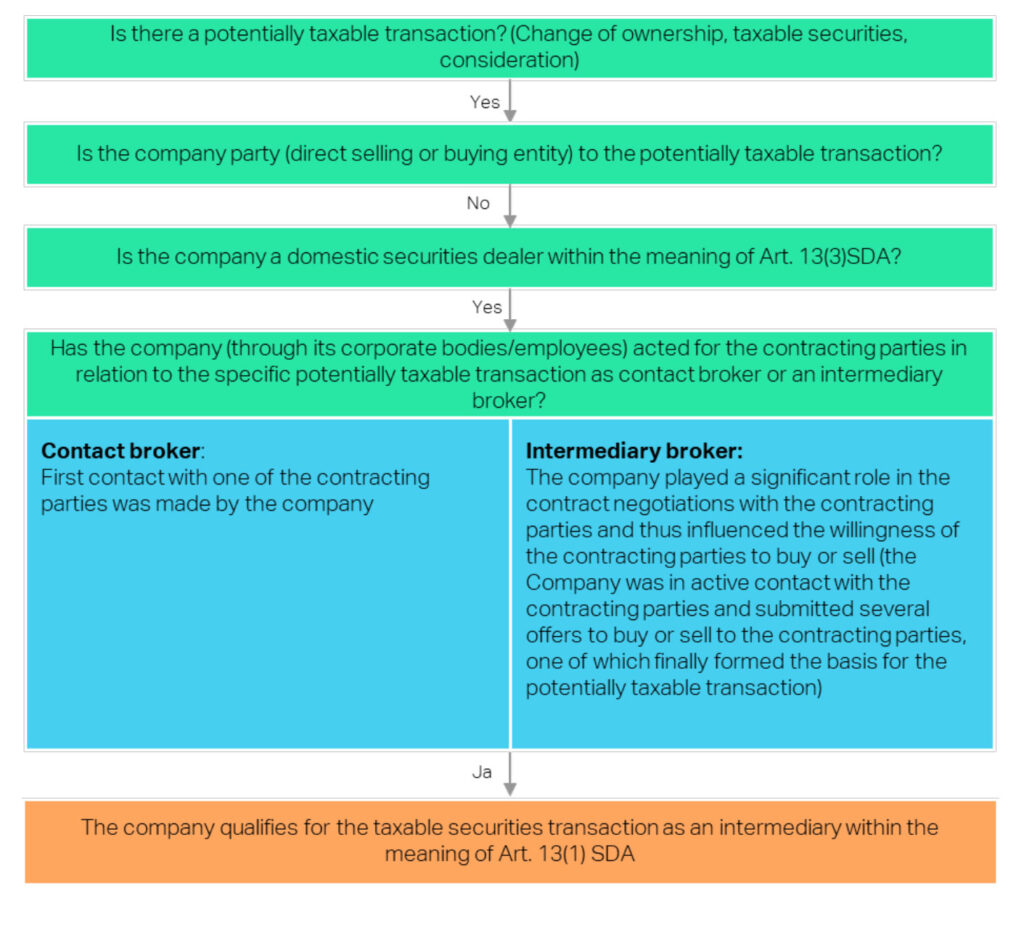

3) Securities dealer as an intermediary

A transaction involving a securities dealer as an intermediary may be subject to Swiss securities transfer tax. In its decision of 25 February 2021 (BGer 2C_638/2020) the Federal Supreme Court ultimately concluded that the interpretation of the term “intermediary” in the Stamp Duty Act is to be based on a view borrowed from civil law. The interpretation should therefore be based on the law on brokerage contracts. According to the aforementioned decision, a securities dealer qualifies as an intermediary under the Stamp Duty Act whenever he acts in one of the following capacities in connection with a specific transaction:

– as a contact broker (“Nachweismäkler“), the first person to offer the opportunity to purchase or sell taxable securities (e.g., the first contact with future buyers / sellers of the taxable securities is made by the contact broker);

– as an intermediary who has a significant role in the contract negotiations with future buyers/sellers of taxable securities and has influenced the intention of the contracting parties in a way that was co-determining for the decision to sell/buy (e.g., the intermediary broker leads the contract negotiations with the future buyers/sellers; “Vermittlungsmäkler“).

If a legal entity acts as an intermediary, it acts through its corporate bodies and employees. The economic interests of the securities dealer involved in the transaction and the legal relationships with the contracting parties are thereby irrelevant. The following assessment shows in summary when a securities dealer domiciled in Switzerland qualifies as intermediary:

4) Intermediary as securities dealer

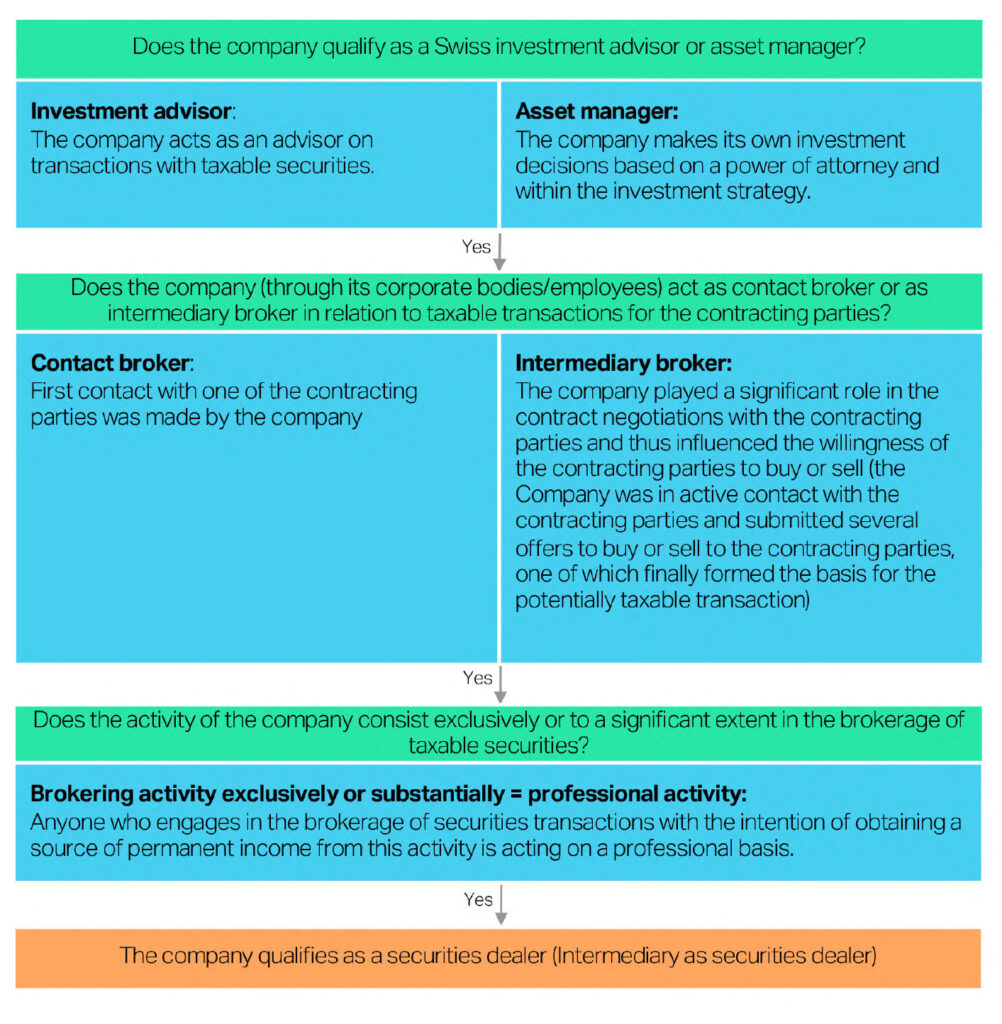

In order for an intermediary to qualify as a securities dealer, the following constituent elements must be cumulatively fulfilled:

– Personal characteristic (“investment advisor or asset manager”)

– Qualitative characteristic (“intermediation of taxable securities”)

– Quantitative characteristic (“exclusively or to a substantial part”)

a) Activity as investment advisor or asset manager

According to the practice of the Swiss Federal Tax Agency (FTA) as well as case law of the Federal Administrative Court, both the terms investment advisor and asset manager are to be interpreted broadly. In its decision of 23 November 2021 (A-5038/2020) the Federal Administrative Court ultimately concluded that anyone who advises on transactions with taxable securities is basically an investment advisor. The investment advisor – in contrast to the asset manager – is characterized by the fact that he only provides advice while the client makes the investment decisions himself. Accordingly, asset managers make buy or sell decisions for their clients and route these orders to a dealer, exchange, or other counterparty.

b) Intermediation of taxable securities

In its decision of 23 November 2021 (A-5038/2020) the Federal Administrative Court ultimately concluded that the interpretation of the term Intermediation is to be based on a view borrowed from civil law. It requires an activity that qualifies under civil law as contact brokerage (“Nachweismäklerei“) or intermediary brokerage (“Vermittlungsmäklerei“). The contact broker is the first person to offer the opportunity to purchase or sell taxable securities (e.g., the first contact with the future buyers/sellers of the taxable securities is made by the contact broker). An intermediary broker plays a significant role in the contract negotiations with the future buyers/sellers of taxable securities and has influenced the intention of the contracting parties in a way that was co-determining for the decision to sell/buy (e.g., the intermediary broker leads contract negotiations with future buyers/sellers). If a legal entity acts as an intermediary, it acts through its corporate bodies and employees.

c) Exclusively or to a substantial part

According to case law (A-5038/2020) and practice of the FTA, the criterion that the activity must consist “exclusively or to a substantial part” in intermediating the purchase and sale of taxable securities is not important. In particular, it is not required that this activity predominates in terms of time. As a result, the case law and FTA focus on “professionalism”. In particular, anyone who intermediates securities transactions with the intention of obtaining a permanent source of income from this activity is acting on a professional basis. In this respect, neither the number or value of the intermediated transactions, the effort expended for this purpose, the turnover or profit achieved, nor their percentage share in the total turnover or total profit of the intermediary is relevant. The case law leaves it sufficient that the intermediary is profit-oriented.

d) Assessment scheme according to current practice

The following assessment shows in summary when a company domiciled in Switzerland qualifies as a securities dealer due to intermediary activities:

5) Implications for Swiss intragroup management companies and Swiss Single-Family Offices

In view of the case law of the Federal Administrative Court, it is not surprising that the question arises whether Swiss management companies in which M&A departments of groups are located qualify as professional intermediary and therefore as securities dealer.

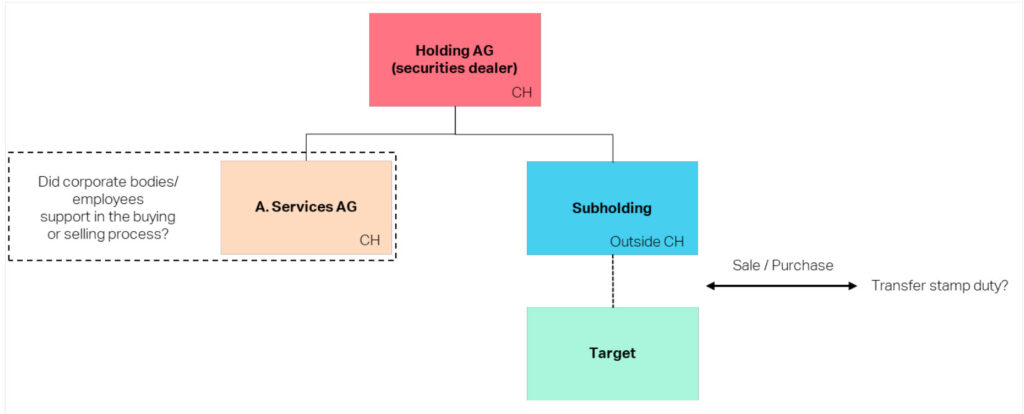

Example 1: A.Services AG is a profit-oriented group service company based in Switzerland. A.Services AG provides its services exclusively within the Group. A.Services AG’s M&A employees account for only about 5% of the total workforce. These M&A employees conduct contract negotiations on behalf of the buying or selling Group company, sign letters of intent (LOI) and are authorized to conclude share purchase agreements for the buying or selling Group companies. A.Services AG renders its services to Group companies, which pay A.Services AG for these services a cost-plus compensation. A.Services AG (or its corporate bodies/M&A employees) advises the group companies with regard to transactions with taxable securities and thus basically fulfills the definition of an investment advisor. In addition, A.Services AG acts as an intermediary as it conducts the contract negotiations on behalf of the buying or selling group companies. Since A.Services AG is a profit-oriented company, it also carries out the intermediary activity “to a substantial part”. According to the current practice of the FTA, A.Services AG thus qualifies as an intermediary and securities dealer (Art. 13(3)(b)(2) SDA). It should be noted, however, that even if A.Services AG qualifies as a securities dealer according to the FTA, each individual transaction must be examined to determine whether A.Services AG actually acted as an intermediary. If the M&A team of a foreign group company has conducted the contract negotiations in a specific transaction and A.Services AG has, for example, only performed the due diligence, A.Services AG does not owe any Swiss securities transfer tax on this transaction (Art. 13(1) SDA).

The same questions arise for Swiss Single-Family offices, as the following example illustrates:

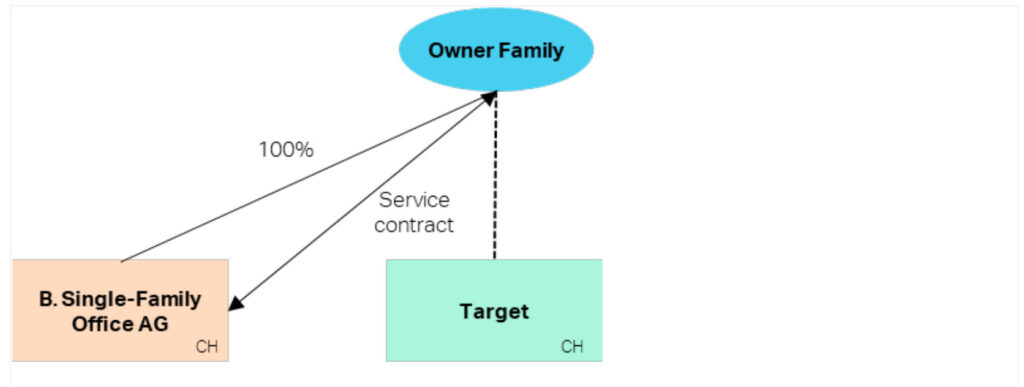

Example 2: B.Single-Family Office AG is a profit-oriented family office domiciled in Switzerland. The family office is 100% owned by the owner family. The family office has ten full-time employees, of which one full-time employee deals exclusively with advice and decision-making regarding equity investments and divestments. This employee also conducts contract negotiations with potential buyers and sellers on behalf of the members of the owner family and is authorized to make the investment or divestment decision and to sign the purchase or sale contract. B.Single-Family Office AG provides its services exclusively to the owner family or to companies affiliated with the owner family, which pay B.Single-Family Office AG a compensation for these services calculated according to the cost-plus method. B.Single-Family Office AG (through its corporate bodies/employees) advises the members of the owner family or affiliated companies with regard to transactions with taxable securities and makes investment decisions on the basis of a power of attorney and thus basically fulfills the concept of an asset manager within the meaning of Art. 13(3)(b)(2) SDA. In addition, B.Single-Family Office AG acts as an intermediary by conducting contract negotiations. Since B.Single-Family Office AG is a profit-oriented company, it also carries out the intermediary activity “to a substantial part”. According to the current practice of the FTA, B.Single-Family Office AG thus qualifies as an intermediary within the meaning of Art. 13(3)(b)(2) SDA. It should be noted, however, that even if B.Single-Family Office AG qualifies as a securities dealer according to the FTA, each individual transaction must be examined to determine whether B.Single-Family Office AG actually acted as an intermediary within the meaning of Art. 13(1) SDA. If a member of the owner family has conducted the contract negotiations in a transaction himself and B.Single-Family Office AG has, for example, only performed the due diligence, B.Single-Family Office AG does not owe any Swiss securities transfer tax on this transaction.

6) Implications for Swiss group parent company as intermediary

a) Intermediary activities of a Swiss group parent company as securities dealer

In most cases, the Swiss group parent company qualifies as a securities dealer, as it has taxable securities in excess of CHF 10 million on its balance sheet (Art. 13(3)(d)). In view of the case law of the Federal Supreme Court, it is not surprising that the question arises as to when the Swiss group parent company becomes an intermediary within the meaning of Art. (13)(1) SDA in certain cases.

In this context, only the conduct of the natural persons of the securities dealer involved in the contract negotiations is relevant. Thus, the group parent company is involved in intermediary activities if corporate bodies and/or its managing director initiates the transaction as contact broker or if a natural person in the securities dealer’s M&A team (or other employees) substantially participates in the negotiations and in the conclusion of the contract (intermediary broker). For the attribution of acts, it is neither necessary nor sufficient in itself that the person in question can legally represent the group parent company. The authority to sign for a person involved in contract negotiations, which is recorded in the Commercial Register, is therefore typically an indicator that these persons had a corporate body or employee function within the securities dealer, which justifies attributing their actions to the securities dealer. What is directly relevant, however, is whether the persons involved in the negotiations actually held, or at least appeared to hold, a corporate body/management/executive or employee function at the securities dealer and acted in the performance of this function (2C_638/2020).

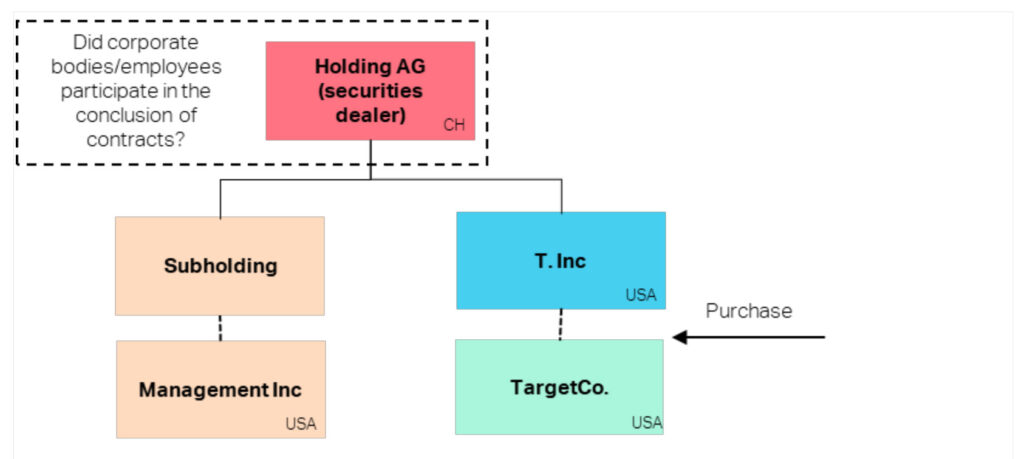

Example 3: Holding AG is a securities dealer and Swiss parent company of an international group which holds various domestic and foreign group companies. An indirect foreign subsidiary, T. Inc. (USA), acquires a target company in the USA, TargetCo. The negotiations with the sellers of TargetCo are conducted by the CEO and CFO of Holding AG, who also signed the SPA on behalf of Holding AG. Since the CEO and CFO of Holding AG conducted the negotiations in their functions as CEO/CFO of Holding AG and also signed the SPA on behalf of Holding AG, Holding AG is involved in the purchase of TargetCo as securities dealer and intermediary. The taxation requirement of Art. 13(1) SDA is thus fulfilled and the Swiss securities transfer tax of 0.3% on the market value of the shares in TargetCo must be paid.

Variant: The contract negotiations were conducted by the CEO/CFO of the foreign Management Inc. of Holding AG and the SPA was signed by the CEO/CFO of the Management Inc. for Holding AG and T. Inc. (both as contracting parties). Under the signatures on the SPA for Holding AG was the designation “CEO/CFO of the Group Holding AG”. Both CEO and CFO held formal positions at Management Inc. and were employed exclusively by Management Inc. In the e-mail signatures of the CEO/CFO, their position was referred to as “CEO/CFO of the Group Holding AG”. In the contract negotiations, both CEO and CFO appeared as “CEO/CFO of the Group Holding AG”. Neither the CEO nor the CFO were corporate bodies/employees of Holding AG. However, according to Swiss Federal Supreme Court, the appearance that the CEO/CFO acted for Holding AG and not for Management Inc. is sufficient. Since both the CEO and the CFO signed the SPA on behalf of Holding AG and acted on behalf of Holding AG vis-à-vis the sellers by naming the function CEO/CFO of the Group Holding AG, the appearance was created that the CEO/CFO acted on behalf of Holding AG (“Anscheinsvollmacht“). Thus, Holding AG was involved in the purchase of TargetCo. as a securities dealer and intermediary. The taxation requirement of Art. 13(1) SDA is thus fulfilled and Holding AG must pay the Swiss securities transfer tax of 0.3% on the market value of the shares in TargetCo.

b) Structuring options to avoid qualification of the parent as intermediary

If the persons involved in material contractual negotiations are employees of a foreign group company (e.g. a management company of the group) who do not hold a corporate body function of the group parent company, the group parent company does not qualify as intermediary broker. If only the foreign management company is active in a transaction (initiating the transaction by searching for potential buyers/sellers, signing the LOI, conducting the contract negotiations, etc.), the acquisition is not subject to Swiss securities transfer tax for the group parent company. The decisive factor is that the group parent company does not make any external representations to potential buyers and sellers in connection with the transaction from the very beginning. The activities of natural persons who act as agents or intermediaries for the management company can only be attributed to the group parent company if they (i) actually or apparently exercise a management, executive or employee function at the group parent company and (ii) acted for the group parent company in the performance of this function.

If persons signing on behalf of the management company are also authorized to sign on behalf of the group parent company, it must be clearly expressed for which group company they are signing in the specific transaction. The CEO or CFO of a management company without securities dealer status may accordingly hold corporate body functions at the group parent company but may have acted in the capacity as corporate body for the foreign management company/foreign group company and not for the group parent company. The CEO’s/CFO’s conduct is then not attributed to the group parent company, but to the foreign management company or another group company (e.g. it is evident from the transaction documents or other documents that the executive bodies with dual function have subscribed or acted for the management company or another group company).

Example 4: Holding AG is a securities dealer and parent company of an international group which holds various domestic and foreign group companies. An indirect foreign subsidiary, T. Inc. (USA) acquires a target company in the USA, TargetCo. The LOI or the decision to invest was made by Holding AG. The negotiations with the sellers of TargetCo are exclusively conducted by the CEO and CFO of T. Inc. (not a securities dealer), who also signed the SPA in the name and on behalf of T. Inc. CEO/CFO of T. Inc. acted exclusively for T. Inc. and aren’t corporate bodies/employees of Holding AG. The key terms of the SPA were approved by Holding AG prior to signing. Likewise, Holding AG secured the financing for the purchase of TargetCo. Holding AG did not play a significant role in the contract negotiations. These were conducted exclusively by the CEO and CFO of T. Inc. The initiation of the transaction, the approval as well as the securing of the financing do not qualify as intermediary activities of Holding AG. Holding AG therefore does not qualify as an intermediary for this specific transaction.

7) Conclusion

The extensive understanding of the notion of activity as an “intermediary” in the context of the definition of “Swiss securities dealer” by the Swiss Federal Tax Administration as well as the latest case law of the Swiss Federal Administrative Court has significant practical consequences: Domestic M&A advisors, Family Offices and management companies could potentially qualify as securities dealers in terms of the Stamp Duty Act, as they act as “intermediary” (within the understanding of the Swiss Federal Tax Administration) on transactions involving taxable securities.

Furthermore, Swiss securities transfer tax risks may arise if the domestic group parent company (which typically is a Swiss securities dealer based on its balance sheet) is involved as an “intermediary” in the sale or purchase of taxable securities.

Stefan Oesterhelt (stefan.oesterhelt@homburger.ch)

Miriam Kämpf (miriam.kaempf@homburger.ch)