In this article, the authors provide an update on the changes with respect to the future treatment of risk-absorbing capital instruments under the revised Swiss insurance regulations, following the conclusion of the partial revision of the regulatory framework for the supervision of Swiss insurance undertakings earlier this year. This article serves as an update to the authors’ previous article on risk-absorbing capital instruments, which was published in CapLaw 3/2022 based on an earlier draft of the revised Ordinance on the Supervision of Private Insurance Undertakings.

By Hansjürg Appenzeller / Vanessa Isler (Reference: CapLaw-2023-57)

1) Revision of Insurance Regulations

Several years in the making, the Swiss Parliament finally adopted the partial revision of the Insurance Supervisory Act (Versicherungsaufsichtsgesetz; Insurance Supervisory Act, the ISA, and as revised by the partial revision, the nISA) on 18 March 2022. After several iterations, the amendment of its implementing Ordinance on the Supervision of Private Insurance Undertakings (Aufsichtsverordnung, Insurance Supervisory Ordinance, the ISO, and as revised by the amendment, the nISO) was published in its final form on 2 June 2023. The nISA and nISO will enter into force on 1 January 2024.

While the main focus of the ISA and ISO revisions was not on risk-absorbing capital instruments, it is important to note the significant changes that have been made in the new regulatory framework.

2) Treatment of Risk-Absorbing Capital Instruments under the Old and New Regime

a) Overview over capital requirements of insurers

Insurance undertakings are required to maintain sufficient free and unencumbered capital to cover all of their business activities (article 9 (1) ISA / articles 9 et seq. nISA). This requirement is assessed by way of the Swiss Solvency Test (SST), which, simply put, plots the capital an insurance undertaking should have, quantifying, among others, the market, credit and underwriting risks to which it is exposed (Zielkapital; target capital), against the available regulatory capital (risikotragendes Kapital; risk-bearing capital).

The results of the SST are expressed as the SST ratio (expressed as a percentage. In simplified terms, the SST ratio is calculated by dividing the available capital (i.e., the risk-bearing capital) by the required capital (i.e., the target capital) in a given year. The SST ratio must always be above 100%. In practice, the average SST ratio for insurance undertakings is much higher, amounting to, on average, 303% for non-life insurers, 243% for life insurers and 256% for reinsurers in 2022 (cf. Report on the Swiss Insurance Market 2022, published by the Swiss Financial Market Supervisory Authority FINMA (FINMA) on 7 September 2023).

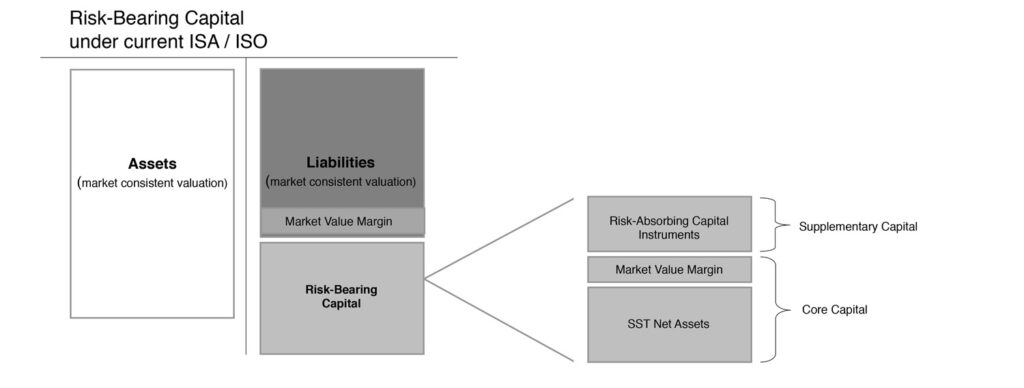

b) Risk-absorbing capital instruments as part of risk-bearing capital

The risk-bearing capital consists of the core capital (Kernkapital) and the supplementary capital (ergänzendes Kapital).

i. Core capital (Kernkapital)

Unter both the old and new regime the core capital is calculated based on SST net assets which are determined using a total balance sheet approach (i.e., the SST balance sheet contains all economically relevant balance sheet items of the insurance undertaking including off-balance sheet items but excluding any corporate tax items), minus certain deductions (article 48 (1) ISO / article 9a (1) nISA and article 32 (3) and (4) nISO).

Although different terms are used to describe the valuation methodology applied to determine the value of the assets and liabilities in the SST balance sheet under the old and new regime (market consistent (marktnah) valuation and market consistent (marktkonform) valuation, respectively), no significant deviations are expected in the valuation of the insurance undertaking’s assets and liabilities in practice.

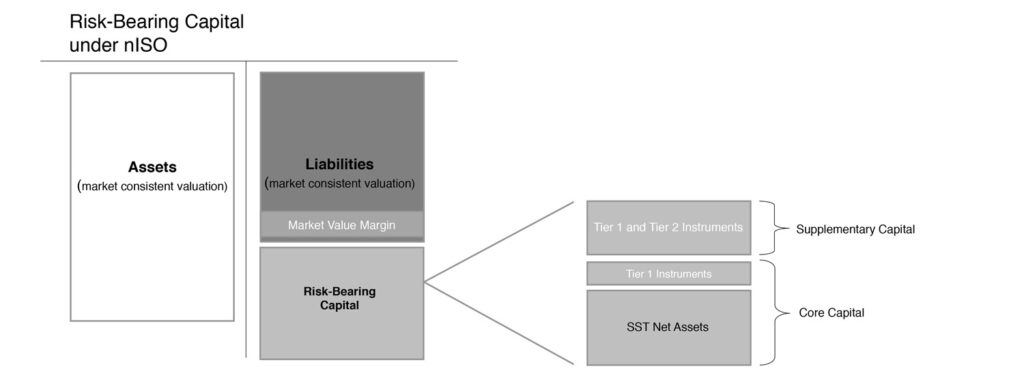

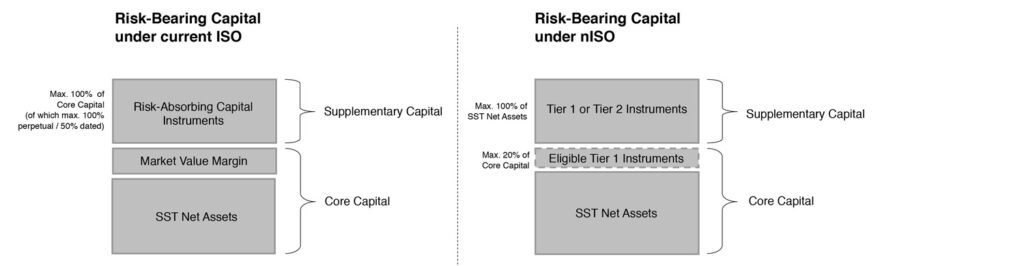

Under the old regime, the market value margin (Mindestbetrag), which is also included in the determination of the market consistent (marktnah) value of liabilities (article 41 (3) and Annex 3 ISO), is added to the SST net assets, positively impacting the calculation of the core capital (article 48 (1) ISO). The market value margin is calculated as the sum of the expected values of the discounted capital costs of each one-year risk capital over the future one-year periods required by the insurance undertaking to fulfil its insurance liabilities. As such, the market value margin is intended to cover the cost of holding the regulatory required capital for the run-off of the in-force business in the event an insurance undertaking ceases business operations. However, it is important to note that, pursuant to the nISO, the market value margin will no longer be added to the SST net assets when calculating the core capital (but is still considered in the determination of the market consistent (marktkonform) value of liabilities, article 30 (4) nISO). Instead, under the nISO, the core capital equals the sum of the SST net assets plus the Tier 1 risk-absorbing capital instruments, to the extent eligible for inclusion in the core capital (cf. article 32 (2) nISO).

ii. Supplementary capital (ergänzendes Kapital)

Pursuant to Swiss capital regulation insurance undertakings have the flexibility to augment their regulatory capital by adding so-called supplementary capital (ergänzendes Kapital) to their core capital. This supplementary capital is comprised of risk-absorbing capital instruments (risikoabsorbierende Kapitalinstrumente), in particular subordinated bonds and loans, which possess certain specific equity-like characteristics (so-called hybrid capital). Risk-absorbing capital instruments can be included in the risk-bearing capital or considered in the target capital.

3) Previous Requirements for the Eligibility of Risk-Absorbing Capital Instruments

The previous regulatory framework distinguishes between upper and lower supplementary capital. Upper supplementary capital (oberes ergänzendes Kapital) is perpetual (i.e., it does not have a fixed maturity date) and can be included in the risk-bearing capital up to a maximum of 100% of the core capital. Lower supplementary capital (unteres ergänzendes Kapital), on the other hand, has an original maturity of at least five years. It can be included in the risk-bearing capital up to a maximum of only 50% of the core capital. In addition, in the last five years of the relevant instrument’s term, the amount eligible for inclusion in the risk-bearing capital is reduced annually by an amount equal to 20% of the original nominal amount of the instrument (articles 47 and 49 ISO).

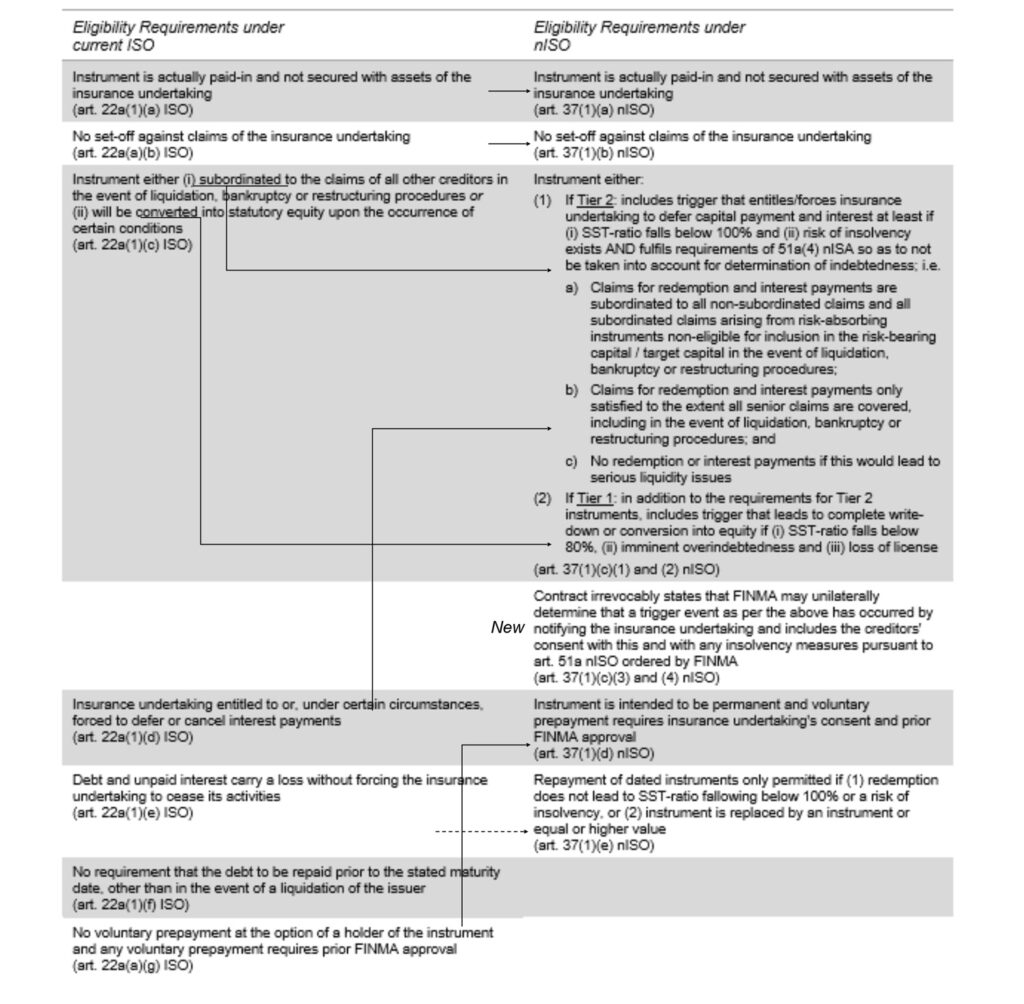

In order to qualify as risk-absorbing instruments pursuant to article 22a ISO and therefore be eligible for inclusion in the insurance undertaking’s risk-bearing capital or consideration in its target capital, the following requirements must be met:

– the instrument is actually paid-in and not secured with assets of the insurance undertaking;

– the terms of the instrument do not allow any set-off against claims of the insurance undertaking;

– the terms of the instrument irrevocably stipulate that it is either (i) subordinated to the claims of all other creditors in the event of liquidation, bankruptcy or restructuring procedures with respect to the insurance undertaking, or (ii) will be converted into statutory equity upon the occurrence of certain conditions;

– the terms of the instrument entitles or under certain circumstances forces the insurance undertaking to defer or cancel interest payments;

– the terms of the instruments stipulate that the debt and unpaid interest carry a loss without forcing the insurance undertaking to cease its activities;

– the terms of the instrument does not in any way require the debt to be repaid prior to the stated maturity date, other than in the event of a liquidation of the issuer; and

– the instrument may not be repaid voluntarily at the option of a holder of the instrument and any voluntary prepayment requires prior approval by FINMA (which shall be granted if the insurance undertaking can show that such prepayment will not jeopardize its solvency).

Not only the issuer of the risk-absorbing capital instrument can benefit from their inclusion in the risk-bearing capital or consideration in the target capital. Inclusion or consideration is also permitted at the group level with respect to the relevant consolidated group SST (article 198 ISO).

4) Changes Proposed for the Eligibility of Risk-Absorbing Capital Instruments

The inclusion of risk-absorbing capital instruments in the risk-bearing capital or consideration in the target capital will remain possible under the nISO. However, the nISO introduces several important changes, primarily aimed at integrating the new restructuring regime for insurance undertakings and increasing comparability with the capital requirements outlined in EU insurance regulation (i.e., “Solvency II”).

5) Separation of risk-absorbing capital instruments into Tier 1 and Tier 2 instruments

Similar to Additional Tier 1 Capital (AT1) and Supplementary Capital (Tier 2 Capital, T2) under the tiered capital requirements for banks set out in the Ordinance on the Capital Adquacy and Risk Diversification of Banks and Securities Firms (Eigenmittelverordnung; CAO), the nISO divides risk-absorbing capital instruments into Tier 1 instruments and Tier 2 instruments.

Tier 1 and Tier 2 instruments differ not only with respect to their maturity, but also based on their capacity to absorb losses while the (re-)insurer remains a going concern (cf. articles 34, 37 and 38 nISO):

| Tier 1 Instruments | Tier 2 Instruments | |

| Maturity | Perpetual (i.e., no fixed maturity date) | Perpetual or minimum maturity of five years |

| Principal loss absorption | Contractually defined conversion into statutory equity or complete or temporary write-down at least if (i) SST ratio falls below 80%, (ii) risk of insolvency exists or (iii) license is revoked | None (but see “Liquidity protection” and “Determination of over-indebtedness” in this table) |

| Liquidity protection | Contractually defined deferral of (re-)payment of nominal amount and interest at least if (i) SST ratio falls below 100% or (ii) there is a risk of insolvency | Contractually defined deferral of (re-)payment of nominal amount and interest at least if (i) SST ratio falls below 100% or (ii) there is a risk of insolvency |

| Inclusion in risk-bearing capital | Can either be included in the core capital (up to a maximum of 20% of the core capital) or be included in the supplementary capital (up to a maximum of 100% of the SST net assets) | Can only be included in the supplementary capital (up to a maximum of 100% of the SST net assets) |

| Determination of over-indebtedness | Treated as liability in determination of over-indebtedness pursuant to article 51a (4) nISA (see below 4) (b)) | Excluded as liability in determination of over-indebtedness only if the requirements pursuant to article 51a (4) nISA are contractually defined and fulfilled (see below 4) (b)) |

Despite the explanatory report to the amendment of the ISO of the Federal Department of Finance dated 2 June 2023 (the Explanatory Report) extolling the virtues of Tier 1 instruments, we do not expect to see a large number of Swiss insurance undertakings issuing Tier 1 instruments in the near future, both due to the increased cost of capital for the issuance of Tier 1 instruments and the limited demand given that Tier 2 instruments can also be included in the risk-bearing capital up to 100% of the SST net assets.

In addition to the introduction of tiered risk-absorbing capital instruments, the nISO no longer includes the market value margin for the calculation of the core capital (see above 2)(b)(i)). Side-by-side the risk-bearing capital under the existing ISO and the nISO looks as follows:

b) Future requirements for the eligibility of risk-absorbing capital instruments

Under the nISO, risk-absorbing capital instruments must still satisfy specific requirements to be considered eligible for inclusion in the core capital or supplementary capital, as the case may be.

Although the eligibility requirements for risk-absorbing capital under article 37 nISO are partially aligned with the existing requirements under article 22a ISO, there are some notable differences to consider. The most significant change is obviously the introduction of two different tiers for risk-absorbing capital instruments (see above under 4) (a)). But article 37 nISO also introduces several other significant changes.

Firstly, in order to be approved by FINMA for inclusion in the risk-bearing capital or consideration in the target capital, risk-absorbing capital instruments have to fulfill the requirements set out in article 51a (4) nISA. This ensures that they be excluded for the purposes of determining the issuer’s over-indebtedness, preventing a situation where somewhat ironically the claims arising from a risk-absorbing capital instrument might themselves trigger an over-indebtedness and undermine the instruments’ loss-absorbing function. However, there is an important distinction with regard to the treatment of Tier 1 instruments. Article 37 (1) (c) (2) nISO states that Tier 1 instruments are treated as a liability in assessing the imminent risk of over-indebtedness and, consequently, whether a write-down or conversion into equity is triggered. As further set out in the Explanatory Report, on a timeline, the Tier 1 trigger event of “imminent over-indebtedness” occurs before the Tier 2 trigger event of “risk of insolvency” (i.e., reasonable concern that on a statutory basis the legal entity’s liabilities are no longer covered by its assets). For both Tier 1 instruments (to the extent they are not written down or converted into equity at that point in time) and Tier 2 instruments, the risk of insolvency triggers a deferral of the repayment of the nominal amount and of interest payments.

Secondly, article 37 (1) (e) nISO introduces a new requirement regarding the repayment of Tier 2 instruments with a fixed maturity. The terms of the instrument must state that repayment is only permitted to the extent that either (i) such repayment does not cause the SST ratio to fall below 100% and does not result in a risk of insolvency or (ii) the instrument is replaced by another (Tier 1 or Tier 2) instrument which is not only of equal or higher quality but also has an equal or more favourable impact on the SST calculation with respect to the amount included in the risk-bearing capital. However, article 37 nISO no longer a priori prevents prepayments prior to the stated maturity date of the relevant instrument (albeit still requiring prior FINMA approval). In this context, article 37 (1) (d) nISO should be understood as an editorial improvement to clarify article 22a (1) (g) ISO without introducing any substantive change.

Thirdly, article 37 (1) (c) (3) and (4) nISO introduce new contractual requirements. The underlying documentation must irrevocably state that FINMA has the unilateral power to conclusively trigger Tier 1 and Tier 2 instruments by notifying the insurance undertaking that a trigger event has occurred. The documentation must also include explicit consent by the creditors to FINMA’s power to unilaterally trigger the risk-absorbing instrument and any other measures FINMA may choose to take in the event of insolvency risks (article 51a nISA).

Pursuant to FINMA’s current practice, risk-absorbing capital instruments may contain a moderate incentive (e.g., interest step up) for repayment without limitations as to the time when such incentive applies. Article 37 (3) nISO codifies this practice for Tier 2 instruments, but such incentive may only kick in ten years after the issue date of the instrument.

Finally, under both article 22a ISO and article 37 (8) nISO, FINMA has the ability to set additional eligibility criteria for risk-absorbing capital instruments to be included in the supplementary capital or considered in the target capital, in particular with regard to assessing the quality of the instruments, their legal enforceability, the fungibility of capital and the default risk of the respectively committed entity. In addition, pursuant to article 37 (8) nISO, FINMA may also impose additional requirements in individual cases. Taking into account the recent comprehensive revisions of the relevant provisions in the ISA and ISO with the legislators stated desire to increase legal certainty and clarity, FINMA should refrain from exercising this authority or at least codify any additional requirements in appropriate form.

c) Eligibility of risk-absorbing capital instruments on group level

Under the existing rules, article 198 ISO allows insurance groups to include risk-absorbing capital instruments in the group risk-bearing capital with respect to the consolidated group SST. Article 198d nISO will introduce more stringent eligibility requirements, but still allows the parent company or another group company to provide guarantees (the Guaranteeing Group Entity) in connection with such risk-absorbing capital instruments.

In order to be eligible on a group level, the instruments must fulfil the following requirements:

– the requirements of article 37 nISO are met with respect to the issuing group company as well as the parent company or group entity (in particular, the Guaranteeing Group Entity);

– the instrument is not secured with assets of the parent company or any other group company (in particular, the Guaranteeing Group Entity);

– the respective Tier 1 or Tier 2 trigger also makes reference to the SST ratio of the consolidated group SST and the insolvency risk of the top group company, as well as any Guaranteeing Group Entity, to the extent applicable;

– to the extent there is an intragroup guarantee, the risk of double payment by the Guaranteeing Group Entity is appropriately limited; and

– appropriate measures are taken to ensure that the risk-absorbing effect is maintained from a group perspective.

By extending the decisive triggers and references regarding insolvency risk to the issuing group company, the Guaranteeing Group Entity and/or the top group company, the revised ISO aims to prevent financial resources flowing out of the group due to payments arising under risk-absorbing capital instruments in situations where the group and the top group company no longer meet the requirements of the consolidated SST and face the risk of insolvency, respectively.

With regard to the appropriate measures to maintain the instruments’ risk-absorbing effect from a group perspective, the Explanatory Report explicitly refers to the measures being adequate and not necessarily absolutely certain.

Further, the Explanatory Report clearly states that risk-absorbing capital instruments may be issued through foreign special purpose vehicles, with the proceeds being upstreamed by way of group-internal loans. This clarification is particularly important given that in practice risk-absorbing capital instruments are often issued via foreign special purposes vehicles for withholding tax reasons.

d) Transitional provisions

Article 216c (1) nISO allows for grandfathering periods for risk-absorbing capital instruments issued and approved as eligible by FINMA under the existing ISO. Instruments that do not meet the eligibility requirements of article 37 nISO can be included in the supplementary capital or considered in the target capital until the earlier of (i) the repayment date and (ii) 10 years following the revised ISO entering into force (i.e., expected to run until 2034).

The draft amendment of the ISO (published on 17 May 2022) provided that risk-absorbing capital instruments issued and approved as eligible by FINMA under the existing ISO, but which do not meet the eligibility requirements of article 37 nISO, are exempt from a bail-in by way of conversion into equity or write-down pursuant to article 52d (4) nISA for a maximum of 10 years following the revised ISO entering into force. This transitional provision has been deleted in the revised ISO. In our view, this deletion should not be interpreted to mean that risk-absorbing capital instruments are not excluded from the conversion and write-down of claims under article 52d (4) nISA. Rather, the later provision should not apply retroactively to risk-absorbing capital instruments issued prior to the adoption of the revised ISA. Otherwise, the legislators’ intent to increase legal certainty and predictability would be undermined.

5) Issues in Practice

Despite not even having entered into force, the revised rules on the eligibility of risk-absorbing capital instruments have already brought to light a number of issues which merit a closer look.

a) Infection risk if eligibility of risk-absorbing capital instrument is revoked during their term

Article 51 (4) (a) nISA discounts risk-absorbing capital instruments from being included in the determination of the issuing entity’s over-indebtedness if they fulfil certain requirements (see above 5)(b)). If FINMA revokes the relevant instruments eligibility, in particular due to the lapse of the grandfathering period for legacy instruments (see above 5)(d)), claims arising out of such instruments (if they do not fulfil the requirements of article 51 (4) nISA) would suddenly be included in the determination of the issuer’s over-indebtedness and could therefore trigger an insolvency event. In practice, however, if such instruments are no longer eligible for inclusion in the risk-bearing capital anymore (e.g., at the end of the grandfathering period), they will likely be called for redemption. The reason being that such instruments would then constitute an overly expensive form of funding.

b) Effect of risk-absorbing capital instruments on the SST

Pursuant to article 34 (1) (a) nISO, the effect of risk-absorbing capital instruments on the SST by inclusion in the risk-bearing capital or consideration in the target capital in terms of amount is determined by (a) the market consistent value (i.e., the financial expenditures of the issuer to fulfil the relevant liabilities; cf. article 27 nISO) on the effective date of the instrument’s inclusion in the risk-bearing capital and (b) the effect on the target capital for consideration in the target capital.

In our view it is not sufficiently clear how the market consistent value of the risk-absorbing capital instrument would be recognized in the SST net assets and eligible with respect to the risk-bearing capital. For instance, if such instrument traded at 80% of its nominal value on the effective date of its inclusion in the risk-bearing capital, article 34 (1) (a) nISO implies that it would only be included to that extent in the risk-bearing capital, but for purposes of the SST net asset calculation added to the liabilities at 100% of its nominal value.

Hansjürg Appenzeller (hansjuerg.appenzeller@homburger.ch)

Vanessa Isler (vanessa.isler@zurich.com)