On 4 November 2015 the Swiss Federal Council has published the Message (Botschaft) on the Financial Services Act (Finanzdienstleistungsgesetz, FIDLEG). In the industry, it has been expected with great excitement and interest, as it will have a major impact, inter alia, on how financial services and products may be offered and sold to clients. Also, the FIDLEG, together with the new Financial Institutions Act (Finanzinstitutsgesetz, FINIG), will define how equivalent the relevant Swiss regulation will be when compared with, in particular, EU regulation. This article aims to provide a short overview on the core content of the FIDLEG, namely, the conduct duties to be complied with at the point of sale.

By Sandro Abegglen / Luca Bianchi (Reference: CapLaw-2016-3)

1) Introduction

As is well known, the new Financial Services Act (FIDLEG) aims to enhance client protection and to establish a level playing field with respect to the regulatory framework of financial services (cp. CapLaw-2015-33, CapLaw-2015-3, and CapLaw-2014-5). The recently published message of the Federal Council to the FIDLEG, which is discussed in the Council of States’ Committee for Economic Affairs and Taxation (WAK-Ständerat) these days, allows for another outlook on the proposed law (which, however, may be subject to further changes). The stipulation of regulatory conduct rules remains a key aspect of the proposed FIDLEG, and apart from a number of general duties that have mainly been transferred from civil law, some new duties concerning the point of sale will have to be implemented by financial institutions.

This article provides a high level overview on the new regulatory conduct rules that will apply to financial services providers under the FIDLEG. It does not further discuss other aspects such as the regulatory product transparency rules on the offering of financial instruments of the FIDLEG (cp. CapLaw-2016-1 and CapLaw-2016-5).

2) The new Regulatory Conduct Rules

a) General Duties

i) Loyalty, Information and Due Diligence Duties

As a general, now also regulatory, principle, financial services providers will be obliged to act in the best interest of their clients and provide the required information, due diligence and care vis-à-vis their clients under the FIDLEG. These general regulatory duties (that are well known from civil law) comprise additional, more detailed regulatory provisions (as described in Paragraph 2) a).

In particular, financial services providers must provide to their clients key information such as their name, address, area of practice, regulatory status, possibility to obtain information on the training and education of the client adviser, and the possibility to initiate a mediation proceeding before an ombudsman.

Furthermore, financial services providers must inform on the offered financial services and the connected risks and costs, their economic ties to third parties that are connected with the offered financial services, the offered financial instruments (including the connected risks and costs), the market offering considered for the selection of the financial instruments, and the type of custody of the financial instruments (as well as the connected risks and costs).

The information set out above must be comprehensible and may be provided to the clients in standardized form and electronically.

ii) Documentation Duties

Pursuant to the message, financial services providers will have to document their services adequately. Moreover, with respect to asset management and investment advisory services, financial services providers will be required to record the client’s needs and the reasons for a recommendation that leads to the purchase, holding or sale of a financial instrument.

In addition, financial services providers will be obliged to deliver a copy of the required documentation to their clients and must inform their clients in detail about the services actually provided.

iii) Duty of Best Execution

The principles of bona fide and equal treatment while processing client orders represent further duties – though not new – that financial services providers will have to implement. Specifically, financial services providers must comply with the duty of best execution concerning financial, temporal, and qualitative aspects. The creation of internal guidelines concerning the execution of client orders will be mandatory.

iv) Duties regarding Securities Lending

Financial services providers are only allowed to borrow financial instruments from client holdings as counterparties or lend them to third parties (securities lending) if the clients agree to such transactions in a separate agreement in writing or another form that allows for text verification. Uncovered securities lending transactions with financial instruments of private clients will not be permitted. This rule reflects the currently applicable practice of the Swiss Financial Market Supervisory Authority FINMA.

b) Duties for the Point of Sale

i) Assessment of Appropriateness and Suitability

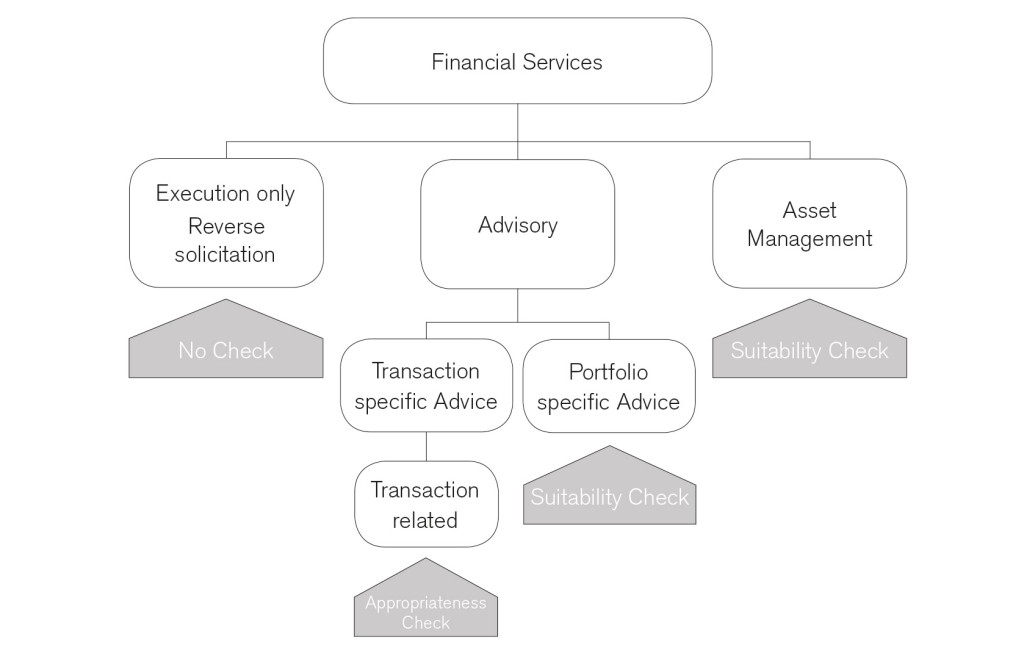

Financial services providers that offer investment advisory or asset management services will have to perform appropriateness or suitability assessments. The following graph describes possible client relationships and the regulatory rules applicable thereto.

(Source: Federal Council, Message on the Financial Services Act (FIDLEG) and the Financial Institutions Act (FINIG), 4 November 2015 version, p. 52, free translation)

A financial institution that provides investment advice (i.e. makes a personal recommendation) for a transaction but without evaluating the complete client portfolio must examine only the appropriateness of financial instruments for the client (duty to perform an appropriateness check). For this purpose, it is obliged to request information on the expertise (knowledge) and experience of its clients with respect to the specific type of transaction that is targeted; should the client lack expertise or experience, such may be produced by appropriate specific information/education.

A financial services provider that renders investment advice under consideration of the client portfolio, or asset management services, must make a suitability check (duty to perform a suitability check). This means that he is obliged to inquire about the financial situation and investment objectives, and also the expertise and experience (like in the appropriateness check) of the clients, before making a recommendation regarding appropriate financial instruments or making respective investments in its function as an asset manager. In case of discretionary mandates, however, appropriateness in our view must only be pertinent in respect of the strategy chosen, not the individual transaction.

Summarized, an adviser or asset manager will only be able to recommend financial instruments or, alternatively, make investment decisions, if the recommendation or transaction, as applicable, is appropriate or suitable, respectively, for the client.

In the context of the above stated point of sale duties, the following exceptions apply:

- With respect to transactions with institutional clients (i.e. regulated financial intermediaries such as Swiss banks, securities firms, collective investment schemes, fund management companies, asset managers of collective assets, asset managers, insurance companies, or foreign financial intermediaries and insurance companies that are subject to an equivalent supervision, as well as central banks), only very selected rules of conduct will be applicable. In particular, vis-à-vis institutional clients neither appropriateness nor suitability checks are required.

- Unless contrary indications arise, professional clients (such as public entities and retirement benefits institutions with professional treasury operations, companies with professional treasury operations, as well as HNWI that opted-out of their private clients status; but excluding institutional clients as set out above) may be deemed to possess the required expertise (knowledge) and experience. They may be looked at as being able to bear the risk of financial services at all times and must be enquired only on their investment objectives.

- Finally, with respect to mere execution only transactions, financial services providers will not be obliged to perform appropriateness or suitability checks. Before executing the services, the financial institutions will have to inform execution only clients that these checks will not be made.

In addition, some of the regulatory documentation and accountability duties will not be mandatory vis-à-vis institutional clients. However, accountability duties that are based on civil law may still be applicable.

ii) Duties related to Product and Fee Transparency

The rules on product transparency will affect both the issuer and the point of sale. For the issuer, compliance with the new prospectus regime will be required. At the point of sale, the basic information sheet (BIB; Basisinformationsblatt) – required basically for all financial instruments other than shares – must be made available to private clients whenever an investment is offered.

Furthermore, the rules on fee transparency described above require the respective appropriate information of the clients, in particular, at the point of sale.

3) Conclusion

Swiss and foreign financial services providers will need to timely implement the new conduct rules. Although many aspects of them are already to be observed today, the granularity of the new regime applicable at the point of sale will require time and effort to implement systems and processes that ensure compliance in an efficient and reliable fashion.

Sandro Abegglen (sandro.abegglen@nkf.ch)

Luca Bianchi (luca.bianchi@nkf.ch)